Founded in 1896, the Kenya Commercial Bank (KCB) Group is an iconic brand in the East African commercial banking and financial services landscape.

With $6.28 bn in assets and operating subsidiaries across seven East African countries, KCB is one of Africa’s largest and most profitable commercial banks, with a market cap of $1.45 bn and international ownership of 29 percent. Euromoney ranked KCB the top bank in Africa in 2015, based on return on assets.

|

David Kitheka, |

For decades, KCB’s investor base included its largest shareholder, the Kenyan Government, and a handful of local institutional and retail shareholders. But as investors became more involved in global markets and Kenya improved its transparency and increased efficiency within its stock market, KCB appeared on the radar of a few foreign emerging market investors. The bank took notice of this attention, and for the first time created an investor relations position to help develop a more global shareholder base.

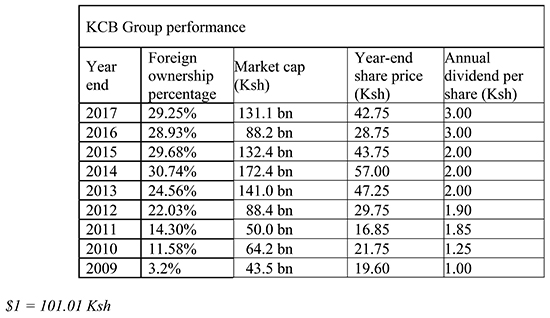

IR activities commenced in 2009, leading to the appointment of David Kitheka as KCB Group’s head of IR. Kitheka is on the front lines managing relationships with investors and shareholders both locally and abroad, particularly in the US, London and South Africa where KCB has been successful in attracting new investor interest. Tellingly, the bank’s share price has more than doubled over his tenure from 19.60 Kenyan shillings (Ksh) ($0.19) at the close of 2009 to Ksh46 at the end of June 2018.

Yet outside of Africa, the continent is widely perceived to be volatile and risky, and as a result investment interest has been limited. So how did KCB Group grow its international ownership by more than 850 percent – from little more than 3 percent to 29 percent – in just eight years?

We spoke with Kitheka about KCB’s investor relations strategy, the political, economic, geographic and financial perception challenges he’s had to overcome, and his goals for the remainder of 2018 and 2019.

1. How did KCB manage the investor relations process prior to creating an official IRO role?

Before creating an official IR position, our investor communications process was generally reactive and unplanned, principally responding to investor inquiries – but, frankly, that was the norm given the limited visibility and investor interest in the bank. The IR effort involved senior management across the company, such as the CEO, credit director, director of strategy and the finance director taking ad hoc meetings and calls only after receiving an investor inquiry.

Not only was this approach inefficient, but it also made it difficult to build and maintain relationships and continuity with investors, with many disparate conversations being held at all levels. With the formation of an IR discipline and department, we have been able to substantially improve the effectiveness and efficiency of our IR effort. Additionally, we have been able to implement a proactive outreach strategy, including regular visits to international money centers, to substantially increase awareness and understanding of KCB.

2. What was KCB’s international shareholder profile when you joined as head of IR?

To give you a feel for what we have achieved at the bank and in our IR program since 2009, I created the table below.

While I’m proud of the progress we have made in diversifying our shareholder base globally, what truly matters to our shareholders is the performance of their investment. There has been a fair amount of volatility in our share price – reflecting a range of factors – but it is gratifying that our year-end share price has more than doubled since we initiated a formal IR process.

3. Tell us about some of the steps you took to increase your base of international investors.

Our strategy was to seek and engage a diverse set of investors that matched the criteria of our investment highlights. First, we actively pitched funds that were watching Kenya and similar emerging markets, but not necessarily KCB, to spread awareness and get on their radar. Second, we approached sector-specific investors in banking and financial services.

We also leveraged our relationships with existing institutional investors to identify other prospects with like-minded interests in emerging market investing and/or a focus on banking and finance. In some cases investors would make introductions and in other cases we would pursue the targets on our own.

Furthermore, we invested resources in identifying and attending relevant global investor conferences to meet potential shareholders in new or existing markets. To make an introduction to KCB as easy as possible, we also prepared an investor factsheet that reviewed our operations and performance. We found this simple step to be immensely valuable in helping to develop initial investor dialogues.

4. What challenges did you confront in pitching to international institutions?

Navigating the sometimes enormous misperceptions and lack of knowledge among investors unfamiliar with Kenya, East Africa or emerging markets in general remains a major ongoing challenge. We quickly recognized that before we could focus on the strengths of our company, we first had to educate many investors on basic facts about Kenya, its government policies and the nature of business on the continent. This also provided us with the opportunity to highlight ways in which business and economic activity here has the potential to move much more rapidly than it does in developed markets.

Beyond that, the fact that our shares trade only on the Nairobi Securities Exchange can make it difficult if not impossible for some investors to participate in our stock. And despite having the second-most-traded stock on the exchange, our daily liquidity remains relatively low compared with companies our size in more developed capital markets. Of course, this poses a challenge for most institutional investors, which look for greater liquidity in their investments, and most definitely limits the number of investors that can consider an investment in KCB.

Additionally, having the Government of Kenya as a majority shareholder was often a source of concern as well as an issue that required elaboration. We had to provide clarity on the extent of the government’s influence on the business, and in most instances we were able to convince investors of the benefits of our stability and long-term growth potential.

It also took time to build credibility and trust with investors by delivering on our goals and predictions. We found it took many investors two or three years of tracking our performance before they became comfortable in becoming an investor in the bank. We put in the work to communicate openly and to get out of the office – and the country – to go meet with investors face to face on a regular basis. Through roadshows and attending conferences we were able to regularly meet with investors in New York, Washington, Boston, Chicago, London, Johannesburg, Cape Town and Dubai. This simple, in-person interaction remains a critical element in building new investment for a company like KCB Group. Without it your chances of success seem very low, in my experience.

All companies face some sort of IR challenge, so it’s important to recognize that investor relations requires a long-term orientation and discipline. There’s no way to accelerate investors’ timetable; you just need to invest the time and resources in building a dialogue, listening to their interests and concerns and then providing consistent and credible communications that address their issues.

And I think a major part of our success has been KCB management’s commitment to visiting our investors in international money centers on a regular basis, as well as the quarterly engagement via conference calls following the publication of results. We have heard from many foreign investors that this continuity and commitment to transparency was a key factor in making them comfortable in becoming a KCB stakeholder.

5. Finally, what does the future hold for KCB’s international IR strategy?

Our strategy largely remains the same. We have made great progress in expanding our international shareholder base, but we all recognize the very real potential to expand that ownership to 40 percent or more from where we ended 2017. We are expanding our discussions to a more strategic view of the bank, industry and market as our track record has demonstrated the ability to weather the occasional bumps and still deliver long-term returns. Further, we see a more engaged function dealing with enhanced reporting and disclosure requirements across the globe.

Globalization seems to be here to stay and that should mean more and more foreign investment across all markets. The attractiveness of foreign markets also increases as valuations grow in developed markets, and investors naturally search for better long-term values. You certainly read about these valuation disparities on a regular basis in most major financial media. I’ll probably need to find a few extra hours in the day to cater to a steadily broadening audience, in order to further expand our foreign ownership, but that’s an easily cured problem with some additional support.

Ultimately, we feel KCB remains a very attractive long-term investment opportunity, a feeling that is echoed by 70 percent of the analysts covering us, who consider our shares undervalued. Looking forward, the goal of our effort is to execute an IR strategy that helps to unlock this value.

Tanya Kamatu is vice president at Catalyst IR and Henry Arcano is an associate at the firm