In a finding pointing to how hard it is to see an IPO succeed over the longer term, Iridium Advisors says just 38 percent of IPOs across the Gulf Cooperation Council (GCC) region were priced successfully – even with the firm using a 20 percent price range to define ‘success’.

Iridium arrived at the figure after looking at how many companies saw a first-day closing price within 20 percent of the offer price, analyzing 457 GCC listings between 2005 and 2021.

The Dubai-based company adds that less than a third (32 percent) of companies traded within a 20 percent range of the offer price during the first 30 days of trading. Five years after listing, 69 percent of companies underperformed their country’s benchmark index.

The findings come as Iridium says 2021 was the best year for IPOs since 2007 and the following financial crisis. Looking at both traditional market debuts and direct listings, Iridium data shows 38 companies entered the market in 2021. The majority of these debuted in Saudi Arabia (21 listings), including nine IPOs on the main market, six IPOs on the small-cap board Nomu and six direct listings.

Saudi Arabia was followed by the UAE with 10 listings: five IPOs and five direct listings. Qatar and Kuwait each saw three listings while Oman recorded just one. Iridium says the strong momentum is expected to continue this year.

‘The increased demand to tap into the primary markets has contributed to a strong pipeline of government-owned and private companies expected to go public throughout 2022 and beyond,’ says the firm in the first of a new series of IPO analysis papers. ‘These plans are built on solid foundations: a buoyant oil price, emerging market index membership and a more benign macroeconomic backdrop.’

Leaving money on the table

Despite the positive outlook, Iridium warns pre-IPO companies to be aware that ‘the objective should not only be to complete the IPO itself, but to prepare the company to generate value for shareholders in the long run.

‘This is often forgotten because during the preparation phase of the IPO, advisers working on the transaction are incentivized to take a different perspective. Their interest lies mainly in a successful IPO day, after which they will soon disappear and move on to the next transaction. Countless companies are surprised when their share price commences a steady decline after the hoopla of the IPO ceremony and the first few quarters of life as a public company.’

Acknowledging that determining the right price for an IPO to succeed ‘without leaving too much money on the table’ can be a challenge, Iridium highlights how different first day ‘pops’ can vary from one market to the next in the region.

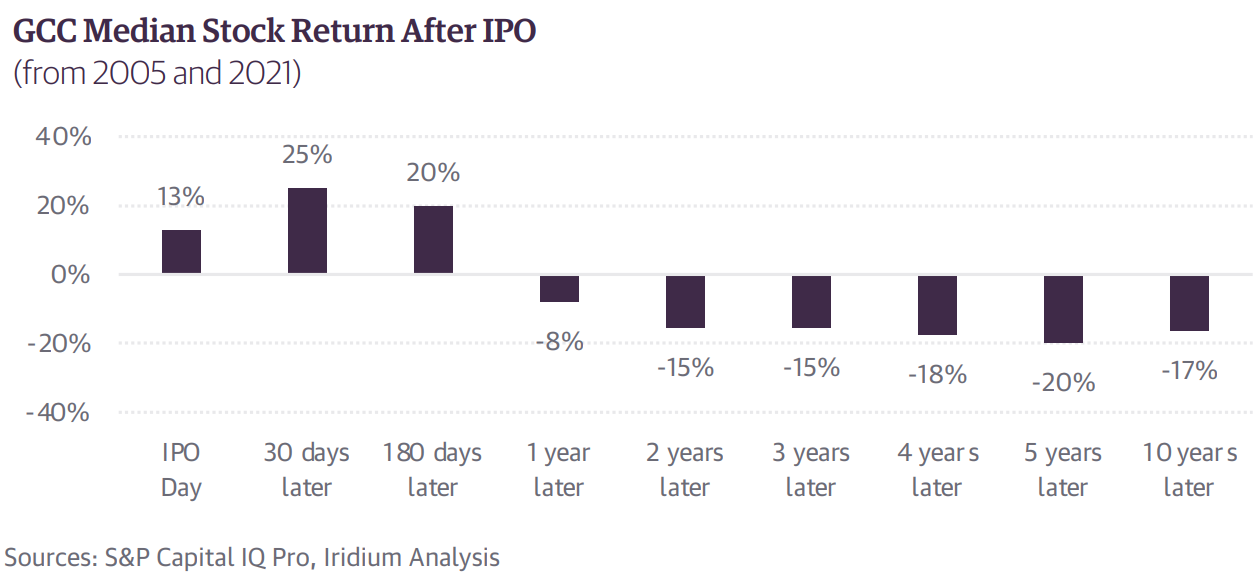

While the median first-day IPO pop across the GCC was 13 percent, there are ‘significant differences’ between markets. For instance, companies in Kuwait (173 percent) and Qatar (109 percent) ‘have left significant amounts of money on the table for investors,’ says Iridium. IPOs in the UAE (25 percent) have left less money on the table, while only those in Saudi Arabia (17 percent), Bahrain (2 percent) and Oman (0 percent) stayed within the 20 percent range.

‘An underpriced offering will usually result in a share price increase on the first day of trading and achieves the objective of creating liquidity in the aftermarket and positive news headlines, but it is not reflective of real IPO success,’ warns Iridium.

Long-term success

Noting that a post-IPO price dip is not necessarily a bad thing, Iridium adds that companies coming to market should take a different view when measuring long-term success.

‘To determine how well a company aligns its interests with its owners, the long-term excess return is a helpful measure,’ it says. ‘The reason is that it offers a relative assessment of IPO success against companies that are already listed.’ Essentially it looks at how the company performed against its country benchmark index – though Iridium also points out that a minority matches or outperforms on this measure.

‘Many company directors and executives will be surprised to learn that 62 percent of all IPOs that listed between 2005 and 2021 underperformed after one year, 67 percent underperformed after three years, and 69 percent underperformed after five years,’ says the firm.

Don’t confuse PR for IR

Among the advice Iridium has for companies considering going public is to be aware of the difference between pre-IPO and post-IPO communications: the difference between PR and IR.

‘PR is the fine art of persuasion,’ says the firm. ‘IR deals in the science and practice of truth. It highlights risks and offers comprehensive data and information to enable market judgment. And it allows the company’s strategy, financial performance and market guidance to be the most persuasive elements for analysts and investors.’

Garnet Roach

An award-winning journalist, Garnet Roach joined IR Magazine in October 2012, working on both the editorial and research sides of the publication. Prior to entering the world of investor relations, her freelance career covered a broad range of...