On the heels of the SEC’s final climate disclosure rule, we can see much is about to change for what companies must disclose to investors. What we now know is that the role of the IRO continues to evolve, with growing expectations in reputation management, ESG and financial communications. More than ever, IROs are the ones responsible for communicating the company’s main messages across many issues.

On the heels of the SEC’s final climate disclosure rule, we can see much is about to change for what companies must disclose to investors. What we now know is that the role of the IRO continues to evolve, with growing expectations in reputation management, ESG and financial communications. More than ever, IROs are the ones responsible for communicating the company’s main messages across many issues.

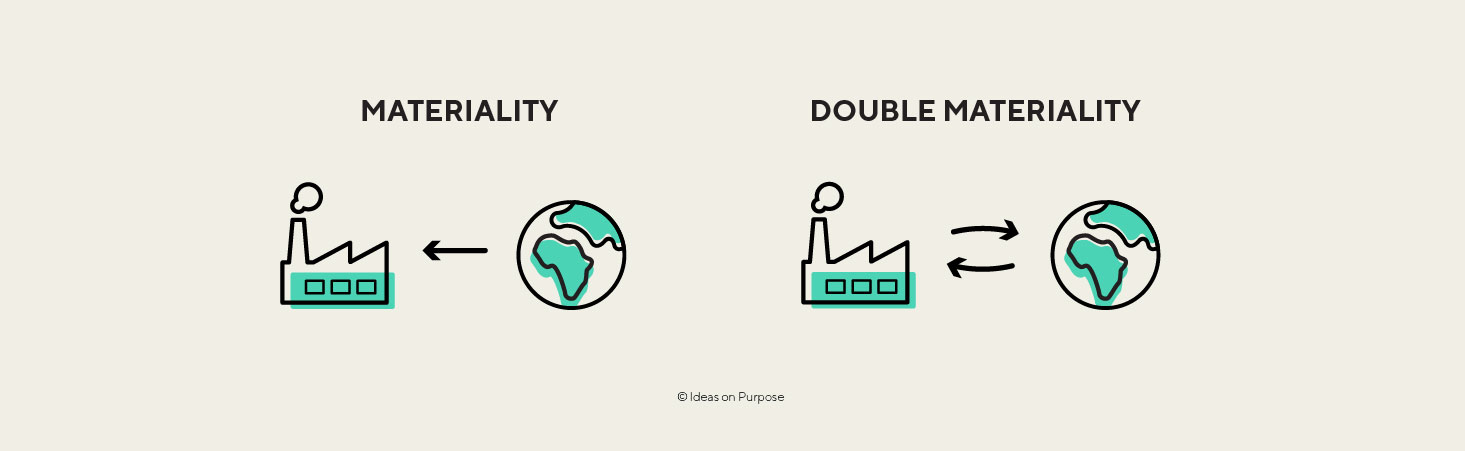

A materiality assessment is typically a financially oriented assessment that identifies and prioritizes broad ESG impacts that can affect a company’s performance, value creation, reputation and legal position. It forms the strategic foundation for ESG planning, budget allocation, risk management and, of course, reporting. Essentially, it’s an assessment of risks and opportunities that might affect the company, the outside-in view. Many reporting frameworks – GRI, TCFD, SASB and the International Sustainability Standards Board (ISSB) – require materiality assessments, and the SEC’s rule requires financial materiality.

What is double-materiality?

Double-materiality adds the dimension of capturing a company’s impact on the environment and communities, adding the inside-out perspective. Assessing ESG impacts from these two angles is what we mean by double-materiality: how a business is financially impacted by ESG topics, also known as financial materiality, and how a business impacts people and the environment (impact materiality).

The concept of double-materiality aims to encourage greater transparency and accountability from companies and promote more holistic decision-making that considers the broader implications of business activities. Most IR professionals have already begun to incorporate some aspects of these dual perspectives, inviting sustainability team members to investor calls and addressing ESG issues in the investor deck. Beyond communications, this shifting lens means potential impacts on internal team structures, external suppliers and stakeholder awareness.

Who’s required to report double-materiality?

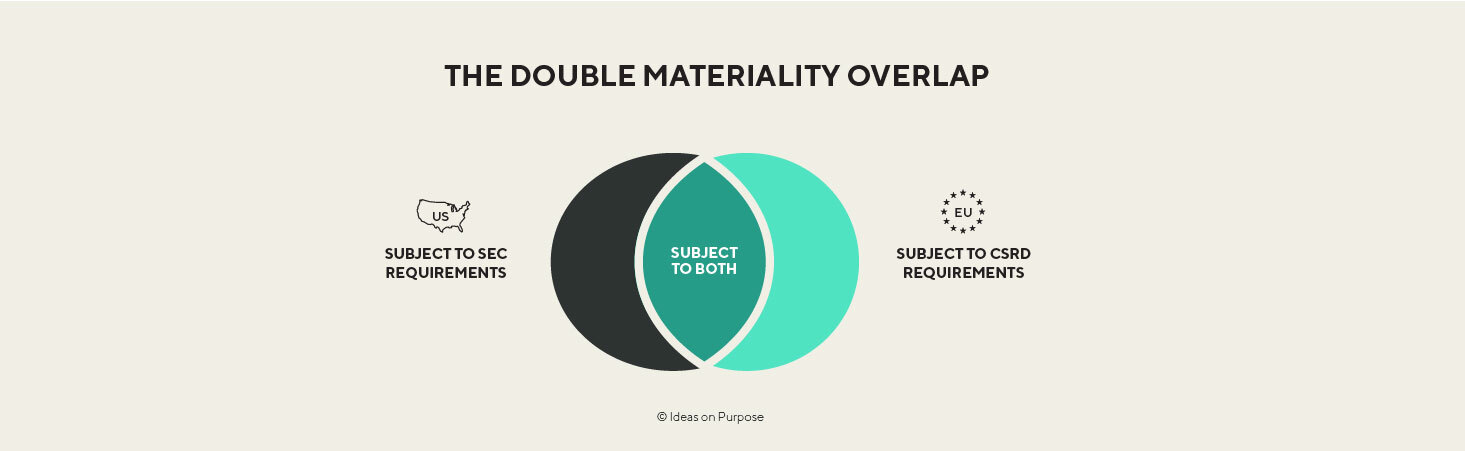

Right now, no US company is required to use this standard. While the concept of double-materiality isn’t new, there has been a huge increase in interest over the last year because it is required for the Corporate Sustainability Reporting Directive, which will reach beyond Europe to US companies with significant business in the continent.

Companies that meet certain thresholds in Europe will be required to report, even private firms of scale. In the US, meanwhile, voluntary reporting has been leaning this way, with GRI embracing it. Some companies will be affected soon, as they fall under required reporting in one or both zones.

What should IR know?

If your company is already reporting with GRI or ISSB, you are in good shape. If you’re just getting started understanding what’s required for double-materiality, here are some helpful tips:

- Assess risks and opportunities regarding the company’s financial value. Much of this is done today in the proxy and 10K

- Ensure your company is identifying relevant sustainability issues. Consider the list of industry sustainability topics from SASB (now IFRS/ISSB) and the European Sustainability Reporting Standards, if applicable

- Look at peers: doing a gap analysis is often helpful

- Look at your company’s impact assessment, or undertake one. Identify the impacts the company has relating to your material topics and the risks and opportunities presented. This requires a company to consider the negative impact of activities, who might be affected and how a negative impact may be avoided or mitigated.

If you’re eager to move toward the new requirements today without sticking your neck out, consider the frameworks that will enable you to be ready from a financial materiality perspective (TCFD and SASB). Working toward these now will put you on the path and give your company enough runway to take care of any operational or data-gathering issues.

And remember: don’t neglect the storytelling and humanity. This is still needed to bring your data to life and ensure your messages are understood with the intended effect.

Michelle Marks is director of strategy and managing partner at Ideas On Purpose

Michelle Marks

Michelle is the principal, strategy and managing partner at Ideas On Purpose, where she leads the development of communication, sustainability, and creative strategies for clients—working across media to ensure all solutions meet business criteria...