What good does it do to have an ideal governance structure if the management of the company isn’t fully behind it? Investors have a clear answer: they prefer to invest in stocks that compare favorably with the rest of the market in terms of both governance structure and corporate management, thus benefiting from a sustainably lower cost of capital.

Violations of the law and deviations from recognized governance norms not only have a negative impact on the value of a company but also make it more susceptible as a target for activist short-campaigns. We have examined the history of such campaigns in Europe and drawn conclusions for portfolio construction, using the European equity market as an example.

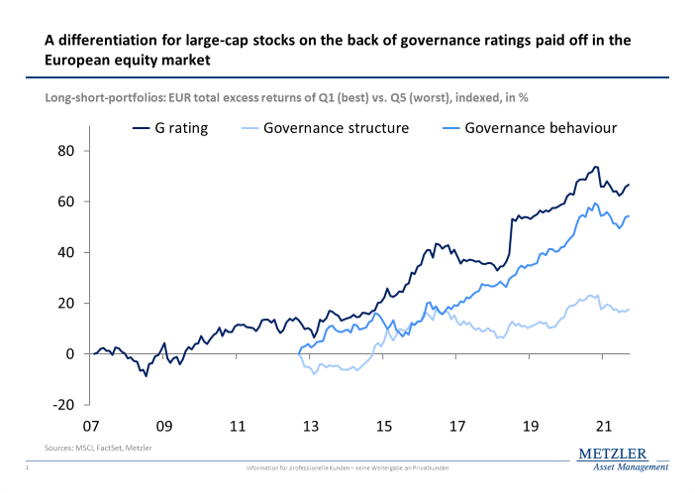

Investors reward best practice governance

Differentiation according to governance factors has sustainably strengthened the risk-return profiles of portfolios invested in European equities. We can also observe that misconduct in corporate management gets punished more severely than an inadequate governance structure.

Governance structure has four aspects: that of the supervisory board, the ownership structure, the remuneration structure and the accounting practices. Governance behavior quantifies business practices in terms of susceptibility to corruption and anti-competitive behavior, taxes and – in the case of financial values – additional aspects of financial market stability

The smaller a company’s market capitalization, the more pronounced this effect will be in retrospect. And that’s because a risk-minimizing governance structure changes in line with the development of a company. The larger and more complex a company becomes, the more important it is to have a strong governance structure in order to keep the risk exposure from value chains and regulations in check.

The assessment of governance behavior, however, is clear: misconduct is always interpreted negatively. As investors expect compliant governance behavior until there is reason to expect otherwise, differentiation according to a company’s actual behavior should be part of portfolio risk management.

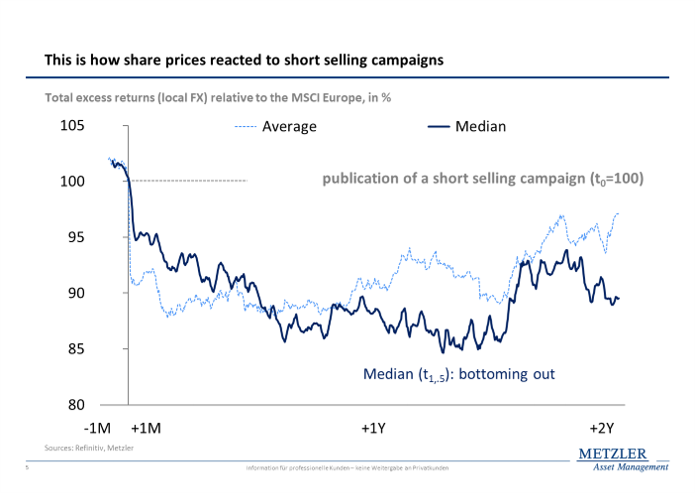

Activist short-campaigns target profiles where governance behavior ratings are low

Activist short-campaigns are a good example of how important it is to avoid weak governance profiles. This insight produces added value especially in the context of concentrated buy-and-hold portfolio strategies that focus on small and mid-caps in the equity market. After all, 90 percent of the almost 100 companies targeted by activist short-campaigns in Europe since 2010 had a market capitalization of less than €20 bn ($22.5 bn).

Sixty percent of these campaigns can be attributed solely to ESG controversies, and the governance category accounted for by far the most cases. Could governance assessments have been used to predict which stocks would be vulnerable targets for activist short-campaigns? A detailed analysis sheds light on this and shows that certain patterns are evident, especially when it comes to assessing governance behavior.

Even if portfolios cannot be completely purged of potential short-campaign targets in advance, historical insight can be translated into preferences that help limit exposure to the most severe cases.

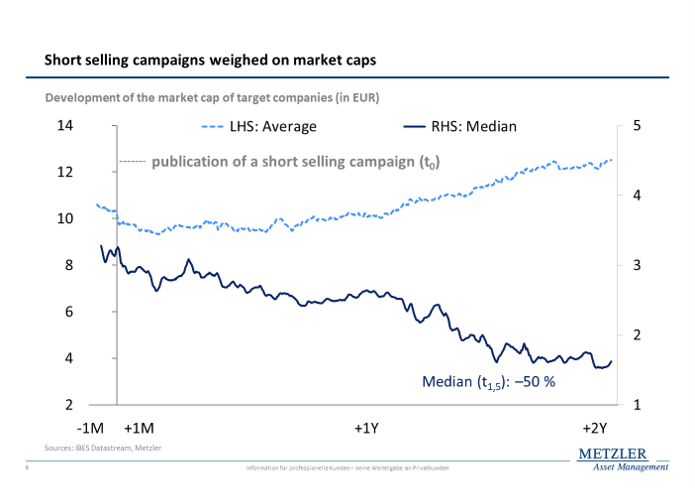

Activist short-campaigns weigh heavily on risk-return profiles

In our research, which is corrected for outliers, gross excess returns on shares in the target companies declined by 15 percent (median figure) compared with the European equity market until they found their floor 18 months after the reports were published. By then, the market capitalization of the target companies had halved. At its peak, aggregate market capitalization of these companies lagged behind by up to €135 bn.

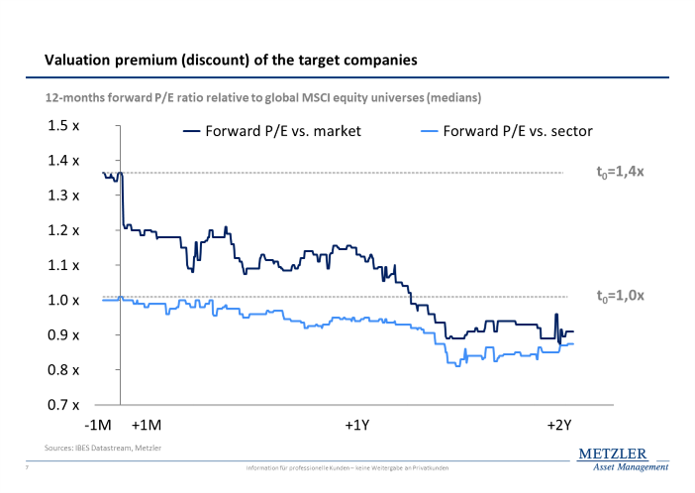

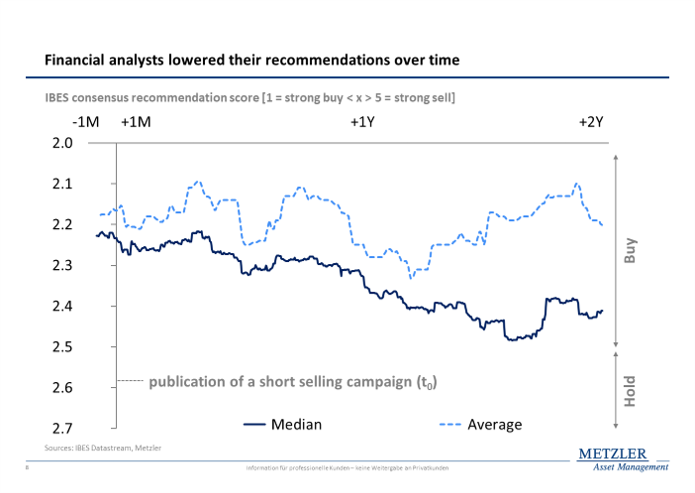

For short-sellers, the campaign is most likely to be successful when its divergence from market expectations is at its greatest so it’s not surprising that almost three quarters of the campaigns targeted companies whose shares were recommended for purchase by financial analysts.

Because financial analysts tend to be organized in industry groups, industry-specific valuation is what they focus on when recommending to buy, hold or sell a certain security. But industry-specific comparisons of valuation multiples give little reason to be more critical of recommendations when it comes to targets of activist short-campaigns. Cross-industry comparisons, however, could have provided an indication of overvaluation.

The success of short-campaigns can be seen not only in the declining share prices, but also when we look at analysts’ recommendations for shares in the target companies over time. Following publication of a critical report in connection with the short-campaigns, analysts tended to successively revise their recommendations downward.

Which investment profile is preferred by activist short campaigns?

The target companies of activist short-campaigns in Europe can generally be described as cyclical growth companies with high P/E ratios and share prices that are more volatile than average. More specifically, we can say that:

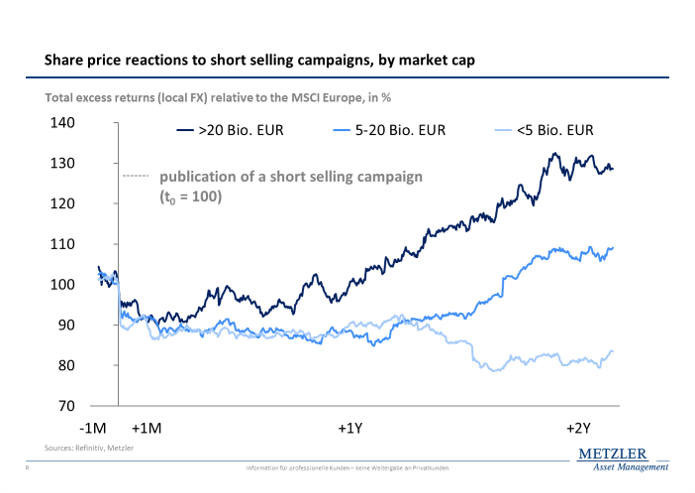

- Large target companies were more likely to recover than small ones: Subdividing the cases in the European equity market since 2010 according to market capitalization at the time of the short-campaigns, we can see that the gross excess returns of all target companies dropped by about 10 percent one month after the publication of a report. Unlike large caps and mid-caps, however, small caps – which accounted for 60 percent of all target companies – did not recover within two years of a short-campaign.

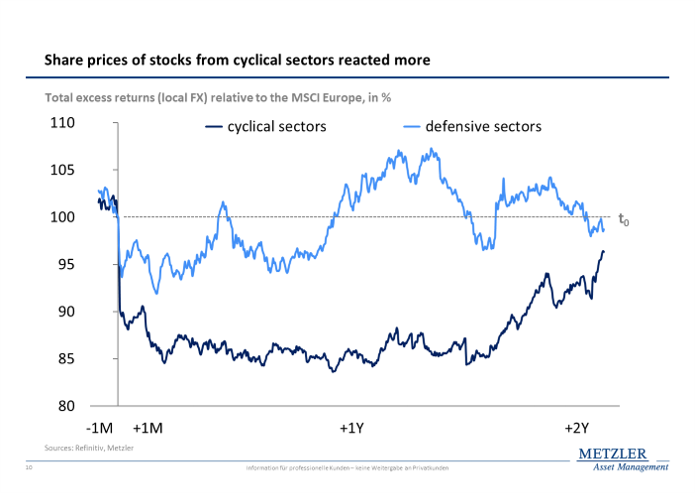

- Cyclical stocks were hit harder than defensive stocks: 75 percent of all target companies were in cyclical sectors. Compared with targets from defensive sectors, the setback in gross excess returns in the first week after publication of a report was -10 percent and thus twice as high. While targets from defensive sectors recovered after just one month, the downturn in cyclical stocks continued for up to 18 months after publication of the respective reports. The most frequently affected sectors were technology (27 percent of cases), consumer discretionary (17 percent) and financials (12 percent).

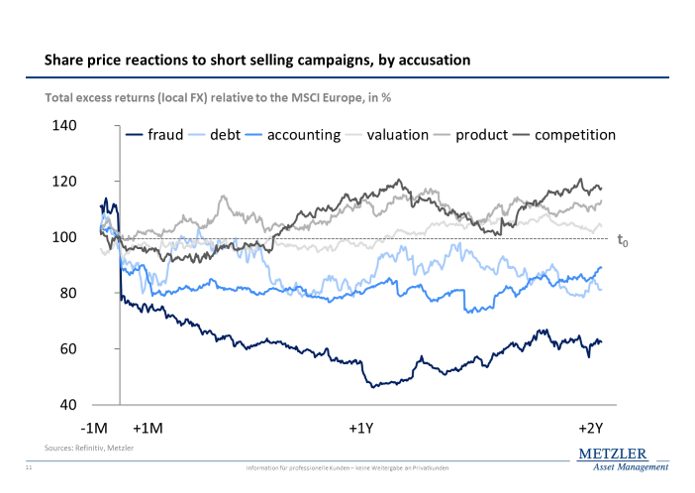

- The nature of the accusation played a decisive role: Where short-campaigns referred to overvaluation (25 percent of cases), poor products (13 percent) and competitive pressure (16 percent), this did not have a sustained negative impact on share prices. Indeed, share prices were most heavily burdened when investors pointed out non-transparent accounting (30 percent) and serious fraud (13 percent) in addition to poor reporting practices. All cases where securities trading was subsequently suspended fell into these categories. Allegations relating to over-indebtedness (3 percent) also led to negative excess returns but accounted for only a small share of the overall pie.

How does this translate into financial KPI profiles?

In retrospect, target companies of short-selling campaigns in Europe can be described as:

– cyclical growth stocks (above market-average consensus analysts’ estimates for sales and earnings per share growth among stocks from cyclical sectors)

– with average-quality properties (above market-consensus analysts’ estimates for earnings per share volatility, higher leverage and lower returns on equity)

– whose share prices had above-average volatility, were accompanied by high P/E valuation multiples relative to the broader market and yet were recommended by the consensus of financial analysts to buy

– with consistently below market-average ratings for governance behavior, a sub-pillar of headline governance ratings next to ratings for the governance structure.

Jan Rabe is co-head of the sustainable investment office at Metzler Asset Management

Disclaimer

This information is not intended for private investors. Metzler Asset Management GmbH does not guarantee the accuracy or completeness of the information presented here. Please see our complete disclaimer at www.metzler.com/disclaimer-mam-en.

Jan Rabe

In his role as co-head of the sustainable investment office at Metzler Asset Management, Jan Rabe is responsible for the integration of ESG into portfolio management and oversees the firm's ESG investment strategy. Prior to his role at Metzler, Jan...