The mounting regulation on corporate reporting of sustainability aspects leads to more transparency, for sure. But this is also becoming a substantial driver of costs for corporates to cope with demands from regulators and investors alike. In particular, smaller, more resource-constrained companies fear that falling behind best practice standards could negatively affect their ESG footprint with ESG rating agencies. This, in turn, could weigh on investor demand for their securities and cause capital costs to rise.

But ESG ratings have become less of a driver of excess returns among European small and mid-cap equities. Knowing that ESG ratings in this segment of the market can be misleading – especially when compared with large-cap peers – investors have turned their attention to two other topics: first, they avoid securities of companies that are repeatedly affected by controversial business practices and, second, they seek to build up impact exposure, such as investing in business models that are aligned with the United Nations Sustainable Development Goals.

A critical approach to ESG ratings is required

When comparing ESG ratings of small and mid-caps with those of large caps in the European equity market, we can see that small and mid-caps are rated at a discount. When ESG ratings are based on a cross-sector comparison using weighted averages for E, S and G sub-components, the mid-point is -5 percent. When sector-specific ESG ratings are used, the discount increases to -15 percent.

Because most investors look at sector-specific comparisons, this puts small and mid-caps at a significant structural disadvantage compared with large caps. The more schematically investors of all-cap products differentiate according to ESG ratings, the greater their preference is for large over small and mid-caps – a misjudgment, we believe.

Smaller companies often do not have access to the same resources as large caps and cannot present their sustainability reporting in a similarly comprehensive and detailed manner. This does not mean small and mid-caps are less sustainable than large caps, but it does mean investors need to take a closer look.

Relying on ESG ratings pays off only to a limited extent

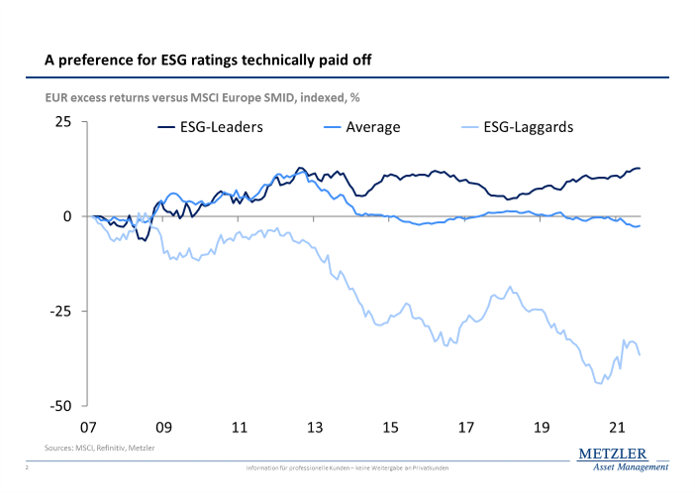

A pure differentiation on the back of sector-specific ESG ratings in the European small and mid-caps segment has been shown to pay off, but this differentiation has been of no great importance. A portfolio of sustainability leader stocks has beaten the market index by just 1 percentage point per annum on average since 2007 – a meager result.

And although a portfolio of laggards fell sharply compared with the market index over the same time period, this played only a minor role overall. This is because these stocks account for only a small share in market capitalization. In the current index universe, this figure is 3 percent.

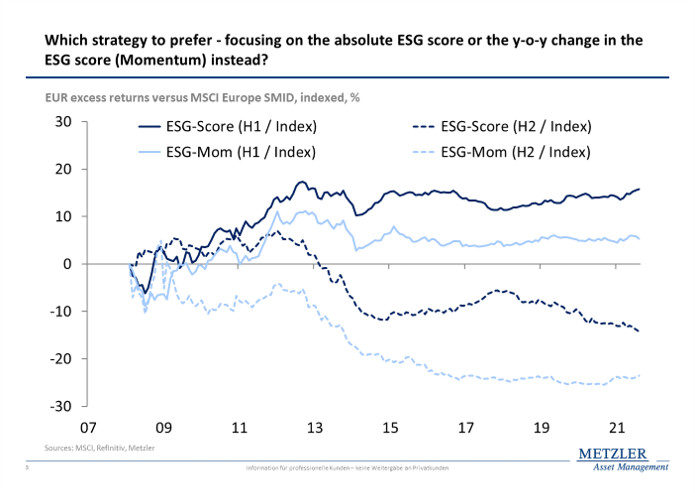

A more refined analysis based on the underlying sector-specific ESG score has delivered slightly higher added value, but since 2011 only for companies to be avoided altogether. A preference for stocks that are associated with either a high ESG score or a positive change in this ESG score (also referred to as ESG momentum) has not delivered significant excess returns compared with the market index in the past decade.

If one replicates the analysis for the three sub-pillar scores of the ESG rating – the E, S and G scores – this leads to the same conclusion. So what really helps strengthen the return-risk profiles of small and mid-cap portfolios?

Avoid stocks that attract negative attention due to controversies

In our experience, owner-managed companies in the small and mid-cap segment pay more attention to reputation than companies in the large-cap segment. In addition, the less complex value chains of smaller companies are also less susceptible to controversy. Moreover, critical NGOs and journalists pay less attention to smaller companies.

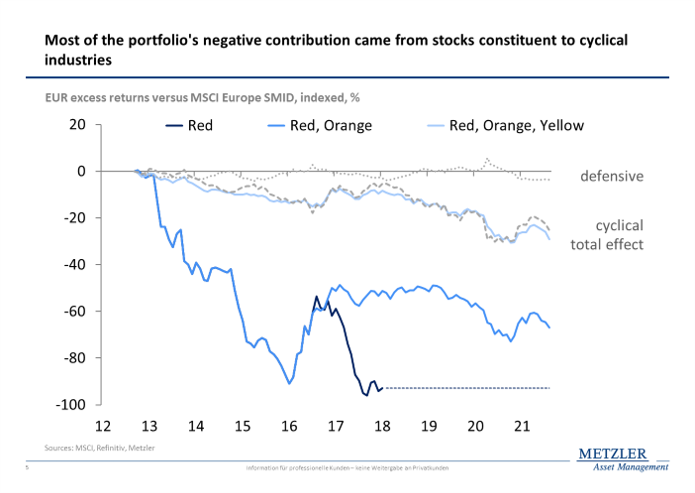

Our analysis reveals that even after controversies have become known, it is still worth avoiding such stocks. Also, the more serious the controversy, the higher the negative contribution to a portfolio. Hence, the risk-return profile of portfolios in the small and mid-cap segment can be strengthened by avoiding stocks that attract attention due to controversies. But which stocks are excluded from portfolios in this way?

An analysis of such risk premium profiles shows that particularly low-growth stocks of lower quality compared with the small and mid-cap segment – those with a weak balance sheet, low profitability or highly volatile earnings profiles – are avoided. Furthermore, sustainable investors do not classify the combination of above-average dividend yield with low valuation multiples as ‘attractive’, but rather as a risk to be avoided.

Invest in stocks with positive impact exposure

So the risks of a small and mid-cap equity portfolio can be reduced by avoiding stocks in companies with weak ESG ratings and controversies. Return potential, on the other hand, can be boosted by investing in stocks that deliver positive impact on the environment and society.

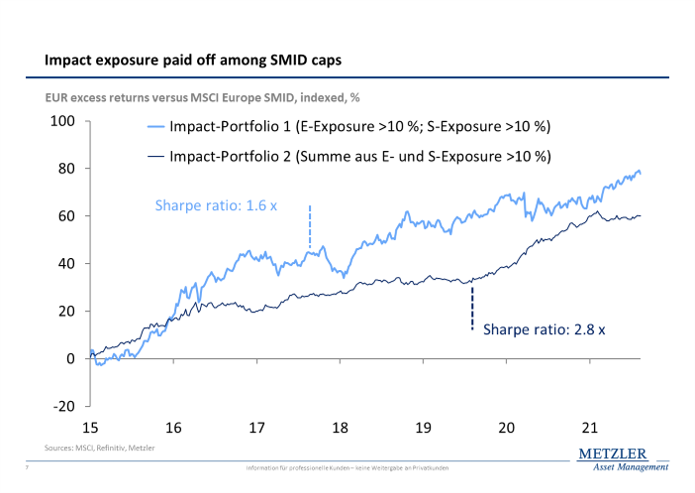

If the volatility of excess returns is taken into account, a portfolio of stocks with significant impact exposure is preferred, irrespective of the contributions from environmental and social categories. Environmental impact exposure has a stabilizing effect here. The excess returns of the stocks with high social impact exposure are lower in comparison and are associated with higher volatility. Put differently, the Sharpe ratio (risk relative to return in percent) of environmental impact exposure is higher than the one obtained for social impact exposure.

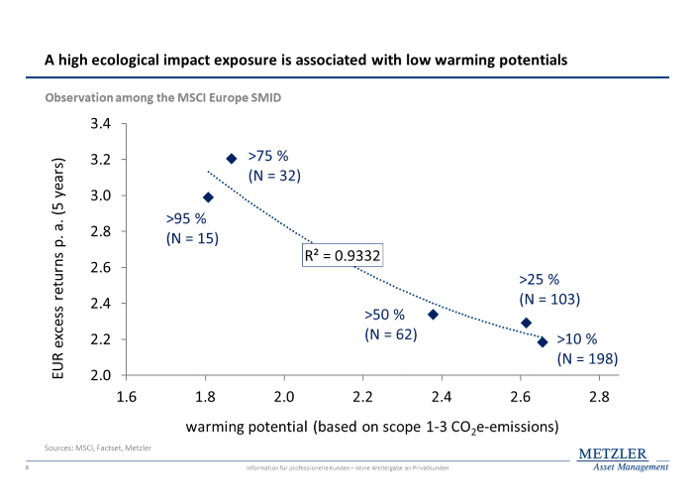

But who says stocks with high environmental impact exposure will continue to contribute to excess returns in the future? We think a lower Scope 1-3 carbon footprint intensity compared with the overall small and mid-cap market could contribute to this, especially when we take into account what impact products and services contribute to both upstream and downstream segments along the value chain. If this carbon footprint is converted into a warming potential using climate models based on the estimates of the UN Climate Council, we can see that their portfolio value (2.7°C) is significantly lower than that of the small and mid-cap market (3.3°C).

The more investment products get aligned with the 1.5°C target of the Paris Climate Agreement, the higher demand will be for stocks with low-warming potential. In retrospect, we see the more pronounced the environmental impact exposure and the lower the warming potential of the companies, the higher the excess return of a portfolio relative to the market.

If this relationship persists, we can assume the impact exposure factor – in particular the contribution from environmental impact – will continue to help stabilize the excess return of such portfolios in the future. Against the background of the upcoming social taxonomy planned by the EU Commission, however, the contribution from social impact exposure shall not be underestimated in the future.

To sum up: The sustainability performance drivers of Europe’s small and mid-caps

If investors want to strengthen the risk-return profile of portfolios in the European equity market by capturing the ‘size’ risk premium, they should focus consistently on sustainability. Four aspects are important here:

- A critical look at ESG data – and ESG ratings in particular – is vital for adequately assessing the opportunities and risks at the stock level. It’s the only way to clarify critical issues with management and achieve added value for the fund

- A pure differentiation on the back of ESG ratings is hardly worthwhile – neither by absolute ESG scores (on which the ratings are based) nor by ESG momentum

- Avoidance of stocks that repeatedly attract negative attention due to controversies reduces a portfolio’s risk exposure

- Return opportunities arise in particular for stocks with high impact exposure. In addition to environmental impact, greater attention will need to be paid to social impact in the future.

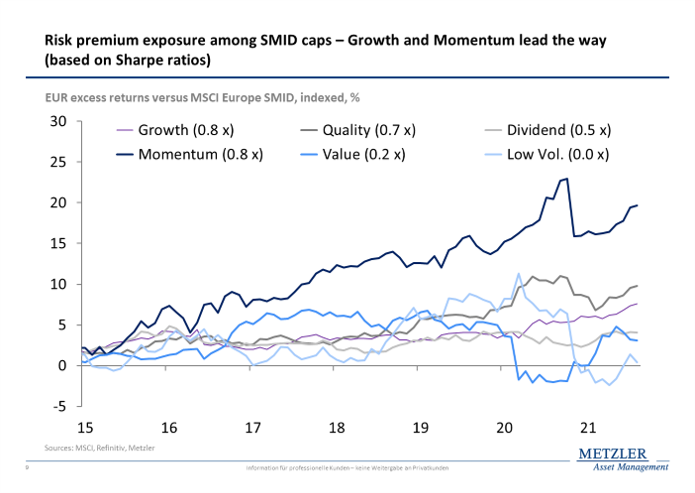

Transferring these preferences to the fundamental analysis of small and mid-caps means investing in stocks of companies that, due to their innovative business models, have pricing power in structurally growing niche markets and thus benefit from high market-entry barriers. With an eye on risk premiums, this means an overweight in growth and quality stocks – a preference that has already been shown to pay off.

The way investors consider sustainability preferences in the small and mid-cap equity segment incentivizes corporate managements to behave responsibly and be aligned with internationally accepted norms and values, such as those outlined by the United Nations. Moreover, it pays off not only to report impact exposure but also to credibly demonstrate how business activities affect the environment as well as society. Business models that do not comply with these standards should find it increasingly difficult to fund operations at a reasonable cost.

Jan Rabe is co-head of the sustainable investment office at Metzler Asset Management. Lorenzo Carcano and Nedialko Nedialkov are portfolio managers for the European Smaller Companies Sustainability fund at Metzler.

Disclaimer

This information is not intended for private investors. Metzler Asset Management does not guarantee the accuracy or completeness of the information presented here. Please see our complete disclaimer at www.metzler.com/disclaimer-mam-en.

Jan Rabe

In his role as co-head of the sustainable investment office at Metzler Asset Management, Jan Rabe is responsible for the integration of ESG into portfolio management and oversees the firm's ESG investment strategy. Prior to his role at Metzler, Jan...

Lorenzo Carcano