If 2020 was the shocker (first) year of the pandemic and all that it entailed, then perhaps 2021 was the year of Covid fatigue. Many in the developed world are now double, if not triple, vaccinated and this year has seen much talk of the return to normal. With the new Omicron ‘variant of concern’ and countries changing restrictions daily, it’s debatable just what that normal is likely to look like, of course.

While we’ve all adapted to our local normal, other issues have clearly shaped the year. Inflation, supply chain issues and an ever-greater focus on ESG and net-zero have been on the minds of investors – and on the corporate earnings call. Nick Mazing, Sentieo’s director of research, takes IR Magazine through a year in charts.

All data supplied by Sentieo. Click on the charts to go to a larger, live version.

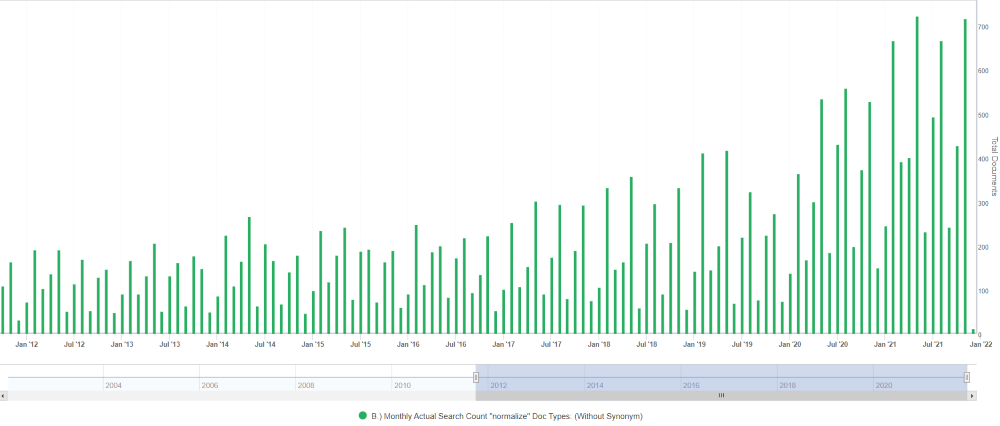

Normalization

The idea of a return to normal was already on the radar in the second half of 2020 and Mazing describes the vaccination rollout across the developed world as giving rise to ‘persistent optimism, despite setbacks’ such as the Delta variant of the coronavirus. ‘We saw more and more transcripts with the word ‘normalize’ in 2021, continuing the H2 2020 trend,’ he says.

Mazing points to a comment from Alan Jope, Unilever’s CEO, on the Q3 call in October: ‘Although life for many of us is starting to normalize, we are operating in a global environment that is far from business as usual. And this is particularly true for Unilever because of our uniquely wide geographical reach.’

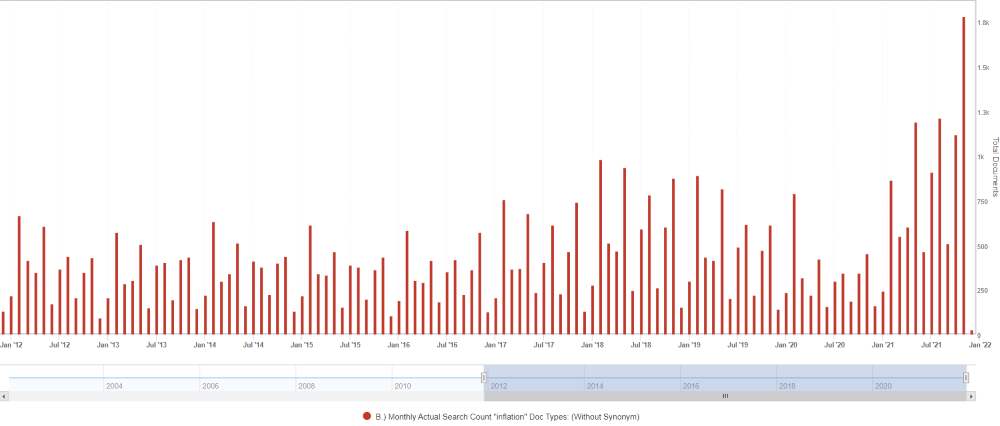

Inflation

Broad-based inflation increased globally in 2021, says Mazing. While central bankers first described it as transitory, he notes that the recently reappointed Fed chairman Jerome Powell suggested it is time to ‘retire’ the word ‘transitory’.

‘Sentieo saw transcripts mentioning inflation jump to almost 2,000 in November 2021, versus a few hundred per month in recent years,’ explains Mazing. He says the November comment from Blackstone’s chief operating officer Jonathan Gray sums it up nicely: ‘I think the biggest challenge by far is what’s happening with inflation. We saw a consumer price inflation number today north of 6 percent. And I think markets and market participants are beginning to realize that this is much more pervasive and likely more persistent than expectations were going back three or six months.’

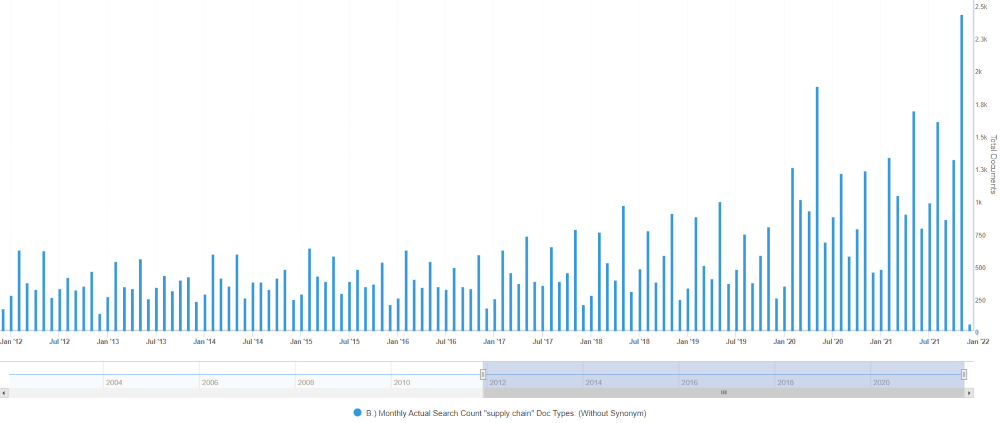

Supply chain

‘Supply chains are a bit like air,’ states Mazing. ‘No one talks about them until for some reason everyone talks about them.’ This was a dynamic Sentieo saw play out during the pandemic twice, he explains: ‘Once in early 2020 as the virus was taking off, and with another spike in the second half of 2021, for different reasons.’

He cites issues around port and factory closures in Asia, backlogs at US ports that became a White House issue, energy supply chain problems in China and Europe, and more. ‘These have resulted in shortages across many industries, from semiconductors and fertilizers to solar panels and, yes, even glass for booze bottles,’ he says.

Mazing selects a quip from Gary Dickerson, CEO of Applied Materials, during the Credit Suisse TMT Conference in November as a nice example of how much supply chain issues have impacted companies: ‘And I can say, I almost feel like I’m chief supply chain officer now. I’ve been in contact with a number of our chip CEO customers.’

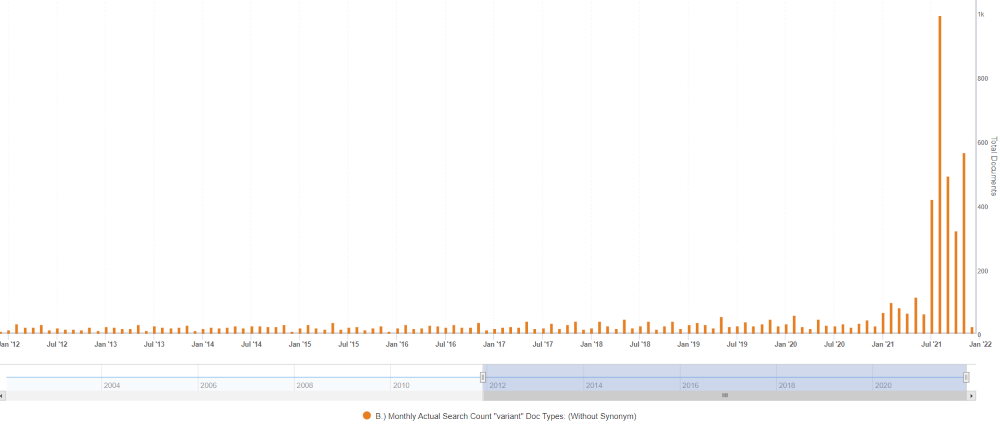

Variant

IR Magazine’s 2020 review pointed to the spike in transcripts mentioning vaccines as pharmaceuticals companies announced the success of their vaccine trials. This year, Covid-19 variants ‘went mainstream,’ says Mazing, with the summer surge in Delta and the more recent spread of Omicron. He adds that while the Delta variant did affect some in-person businesses negatively, data for September and October was more encouraging.

‘And, yes, the unfortunate naming meant Delta Airlines was probably the only company referring to it strictly as the variant,’ says Mazing, picking up a comment from Edward Bastian, the airline’s CEO, during the October call: ‘But as the variant recedes, business travel has picked up over the last month with volumes now reaching the highest level we’ve seen in the recovery. In the last week, our domestic business volume was close to 50 percent restored. We expect continued improvement as offices reopen at the start of the new year, and we anticipate meaningful acceleration in business travel starting at that point.’

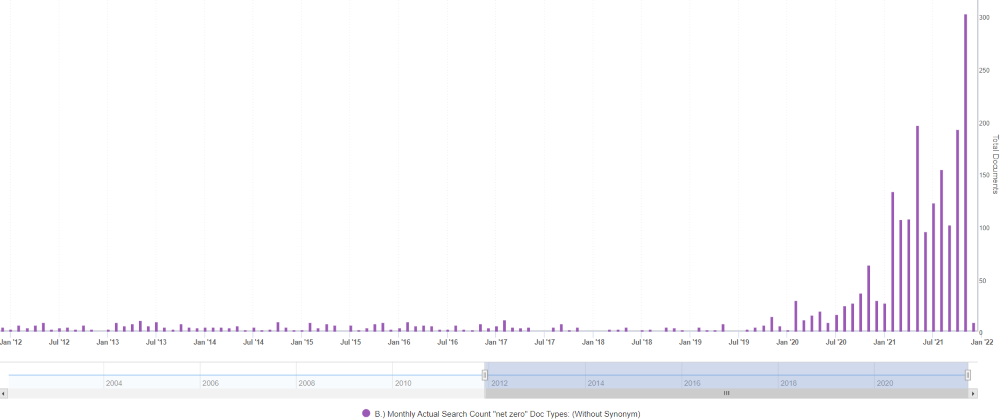

Net-zero

No one could have missed the importance of ESG this year. And unsurprisingly, Mazing says Sentieo has seen ESG topics ‘increasing dramatically in transcripts and filings’.

‘What was interesting about net-zero specifically is that more transcripts in November mention the term than during any other month before,’ he adds, noting that the surge was likely driven by the COP26 events in Glasgow, UK.

As Sanofi’s CEO Paul Hudson outlined in October: ‘Most importantly, we now introduce our net-zero target by 2050. We will take the opportunity of COP26 to set up common initiatives within the industry. Let’s have a quick look at a few key initiatives we’re rolling out. We have set the clear ambition of 100 percent renewable electricity across our operations by 2030. We are moving full speed ahead and delighted to highlight that all our sites in France are now entirely powered by renewable electricity.’

The ‘Covid winners’ lost a lot of ground

Last year Mazing noted the $200 bn market cap gain of four ‘covid winners’: Zoom, Peloton, Teladoc and Slack. This year, ‘the tables have turned,’ he says. ‘While Slack was acquired by Salesforce, we can see the other three companies went from $250 bn aggregate market capitalization in October 2020 – before the vaccine – to less than $90 bn more recently.’

So what happened to the massive pandemic revenue boosts seen by these firms? They’re gone, says Mazing. ‘For example, Zoom’s revenue growth was trending in the high double-digits before the pandemic,’ he explains. ‘Then the pandemic boost accelerated that to a peak of 370 percent in late 2020. This type of growth has now subsided completely: Zoom’s revenue growth in the last quarter was just 35 percent on a year-on-year basis, certainly impressive on an absolute basis but also a far cry from the 2020 numbers.’

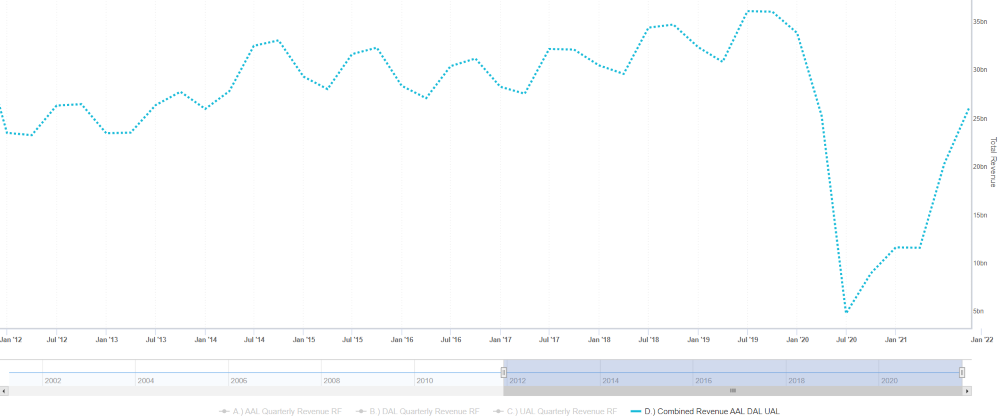

But the ‘reopening winners’ aren’t sailing smoothly, either

While the broad indexes have had what Mazing describes as ‘a great 2021 so far’, what’s happening ‘below the surface’ is that several of the industries that were hardest hit are still struggling to recover to pre-Covid levels. ‘For example, the latest combined quarterly revenues of the big three US airlines – Delta, United and American – is about a third below the corresponding quarter in 2019,’ he says.

OK, so who is winning?

Mazing says the strongest sector in the S&P 500 as at November 30, 2021 was energy, at 50 percent and far outpacing financials, real estate and technology, which were all in the low 30 percent range. ‘At the bottom, we see the traditionally defensive consumer staples and utilities, both below 10 percent year-to-date return,’ he notes.

Garnet Roach

An award-winning journalist, Garnet Roach joined IR Magazine in October 2012, working on both the editorial and research sides of the publication. Prior to entering the world of investor relations, her freelance career covered a broad range of...