The search for capital is not the only reason why western companies are stationing IROs in Asia

When Trevor Schauenberg, GE’s head of IR, took up the role in 2008, the US conglomerate’s shareholder base did not match the global spread of its operations.

‘For a company with 50 percent of revenues and 50 percent of employees outside the US, we felt there was a lot of upside to spending more time with international prospects,’ Schauenberg says.

‘So about a year and a half ago, we added a full-time person in Europe. And then a year ago we added a full-time person for the Middle East and Asia – and he is based in Hong Kong.’

In doing so, GE joined the small number of western companies that, over the last year or so, have stationed a permanent IRO in Asia.

The Asian market holds plenty of appeal to those incorporated elsewhere. This was underlined by a raft of IPOs in Hong Kong last year by non-Asian issuers, which both raised funds and helped cement corporate brands in Asia’s booming economy.

Few companies have taken the step to establish a full-time presence in the region, however. Indeed, when GE was preparing to send its man to Hong Kong, it looked but couldn’t find any similar moves to benchmark itself against.

Early movers include Sanofi, the French healthcare company, which established an IR office in Shanghai 13 months ago, and US telecoms giant Cisco, whose head of international IR moved to Singapore from London last November.

Prada, the Italian fashion house, has an IRO in Hong Kong, the city where it raised $2.1 bn in an IPO last June.

Search for capital

Like GE, Sanofi made the move to boost investment from overseas. ‘With a fast-growing revenue base in Asia, we believe there is an equally fast-growing opportunity to attract investments from institutional investors, including government institutions, in this strategically important region,’ says Felix Lauscher, the company’s Shanghai-based IR officer.

‘As of today, Sanofi already has several significant institutional shareholders, mainly based in Hong Kong, Tokyo and Singapore, representing around 4 percent of our capital.’

Cisco, too, is keen to increase its Asian holdings. But head of international IR Matt Hardwick had other, less obvious reasons to head East.

Within the technology sector, Hardwick has seen US and European investors express an ever-increasing interest in what’s going on in Asia, leading him to conclude that his presence would be more valuable in Singapore than in the UK.

Hong Kong, Singapore or Shanghai?When stationing an IRO in Asia, which is the best city to plump for? GE (Hong Kong), Cisco (Singapore) and Sanofi (Shanghai) all picked their location based on the existing position of regional management. |

As a London-based IRO of four years standing, Hardwick was used to investors stopping in for a chat on the way to see the likes of Nokia in Finland or Ericsson in Sweden. But that began to happen less and less.

‘I had US guys, East Coast and West Coast, saying they were going to Shanghai, or would be in Hong Kong, and could they talk to Cisco’s Asia-Pacific management,’ explains Hardwick. ‘It was really quite an obvious shift.’

Another reason for Hardwick’s relocation was to position IR as a source of competitive intelligence in Asia, as his company believes this is where Cisco’s biggest competitive challenges will emerge in the future.

‘We’ve identified that, over the next five to 10 years, our biggest competitor threat will come out of the Asia-Pacific region. It’s not going to come out of Silicon Valley,’ Hardwick says.

‘If IR is a strategic adviser to the mainstream of the business – not just the C-level executives, but also the top 1 percent of executives across all of Cisco – it seems sensible to have that here.’

Small pickings

For those considering a similar move, it makes sense to have objectives beyond simply raising your Asian holdings. That’s because western companies that target Asia’s capital markets are unlikely to pick up more than single-digit holdings of their shares.

‘It might be 5 percent of your institutional shareholder base,’ explains Nick Arbuthnott, managing director of EMEA at market intelligence firm Ipreo.

While Asia has a significant pool of capital, the amount available to companies from outside the region remains small.

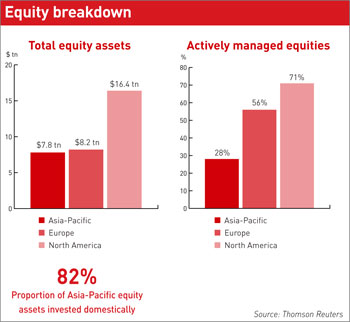

On the face of it, the pool of equity on offer is large and growing fast. Asia-Pacific investors manage a total of $7.8 tn in equity assets, which is nearly as much as the $8.2 tn in Europe, according to a recent report from Thomson Reuters called ‘Asia-Pacific: the investment landscape for investor relations’.

The region also experienced moderate inflows during 2011, while Europe and North America saw funds withdrawn.

But the portion that is actively invested is much smaller in Asia-Pacific: just 28 percent of equity assets are actively managed, compared with 56 percent in Europe and 71 percent in North America, notes Thomson Reuters.

The domestic bias is also stronger in the Asia-Pacific region: more than 80 percent is invested domestically. All this means overseas issuers are chasing a much smaller pool of capital than it first appears.

As Thomson Reuters points out in its report, the majority of capital on offer is concentrated with a small number of investors, including the region’s capital-rich sovereign wealth funds (SWFs).

GE, Sanofi and Cisco all say SWFs were one of the main attractions for setting up an IR office in Asia.

Six of the world’s 10 biggest SWFs – including four Chinese funds – are based in the region and collectively have around $2 tn in assets to play with, according to data from the Sovereign Wealth Fund Institute.

‘If you look at our top 10 international shareholders, historically they have consisted mostly of the Japanese trust banks,’ says Schauenberg.

‘Today that list looks very different, with a large institutional ownership coming from various SWFs throughout Asia and the Middle East.’

Home advantage

Having IR on the ground – while not a prerequisite for investment – certainly helps your cause when targeting Asia’s investors, points out Schauenberg.

‘When I visited in 2009, we had a lot of people interested in meeting with us, but you really need continuity, and I can’t provide that from the US given the time zones and travel limitations,’ he says.

The search for capital in Asia usually takes place through large conferences run by global investment banks in either Hong Kong or Singapore.

One of the main differences between doing IR in Asia compared with Europe or the US is that the big investment bank brands retain a dominant hold on research and corporate access in the region.

‘Those big bank names still mean quite a lot in Asia,’ says Hardwick. ‘The small independent houses that do great research are thinner on the ground here.’

The conference scene, in particular, is different in Asia. Many events have a regional focus, rather than honing in on a particular sector or two, meaning a more diverse crowd and fewer investors ready to buy into your stock.

‘They are big conferences – and I really mean massive – compared with the slightly smaller, more focused conferences we’re perhaps used to in Europe and the US,’ explains Hardwick.

‘You get several industries rather than just industrials,’ Schauenberg adds. ‘There are some exceptions, and those are the ones we try to look for – you want to make sure the investors that are attending are the ones that are going to be interested in your company.’

Like GE and Cisco, Sanofi is on the lookout for more niche events. That’s particularly tough in healthcare, given the strong focus in Asia on the commodity and energy sectors.

Lauscher has found a couple, however, including the China Healthcare Investment Conference – run by Lychee Group, a media firm focused on life sciences – which is held in Shanghai.

Hardwick points out that, while some of the conferences may lack focus, it doesn’t really matter as long as you get the right one-on-one meetings. ‘That’s the most important thing,’ he says.