Since 2015 there has been a significant increase in the number of shares being loaned out by investors across the FTSE 350. In the FTSE 100 we have seen growth of 18 percent (£21.8 bn or $28.7 bn), while the FTSE 250 stock on loan has grown by 26 percent (£8.1 bn).

Stock on loan does not always indicate short-selling activity – think total return swaps, inter-bank lending and banks holdings shares on inventory. In most cases, however, the borrower is hedging against a fall in the share price of the borrowed equity.

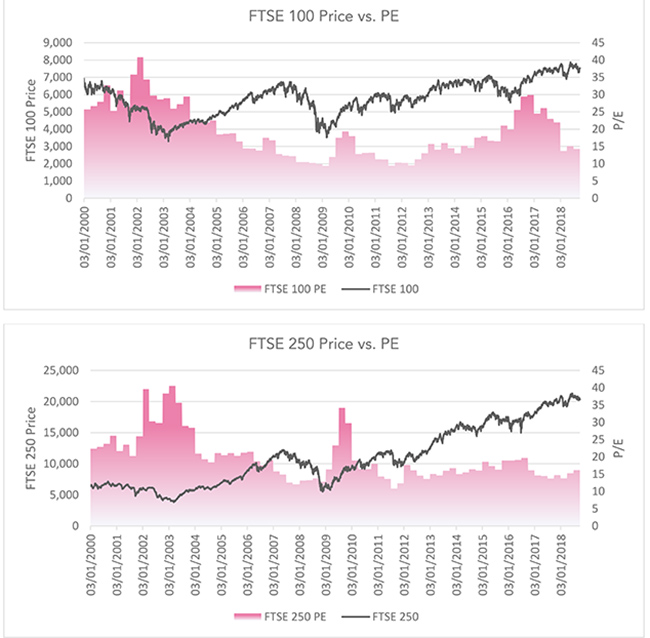

Both the FTSE 100 and FTSE 250 appear cheap when looking at the average P/E ratios over the past 18 years, with both currently being valued at approximately 15x earnings:

What is behind the increase in stock on loan, and where is the liquidity in the lending market coming from?

One of the reasons behind passive investors being able to charge lower fees is the additional revenue stream of securities lending. The rise in passive investing via index and quantitative funds is fueling shorting and stock lending. Quant funds are the driving force, with algorithms automatically opening short positions because of the sheer size of the lending market.

At the end of 2017 the global market of tradable assets stood at more than $20 tn, with more than 10 percent of this being loaned out. The European market alone generated revenues of $2.6 tn in 2017 and expectations are that 2018 produced even higher figures. Of course, it is not just passive investment managers providing the liquidity to the lending market, with active managers seeking returns to cover falling fees in the ultra-competitive asset management market.

There are many cases where investment managers have loaned out their stock unwittingly. In 2002 activist investor Laxey Partners borrowed 42 mn shares in British Land from the market, in order to leverage its voting power in its (unsuccessful) requisitioned shareholder meeting. Hermes Investment Management was one of the contributors to this loan position but did not know this at the time.

This type of action is known as empty voting and, while against the Bank of England’s money market code, it is not illegal – but it has been the focus of attention by the European Securities and Markets Authority in recent years.

Brexit

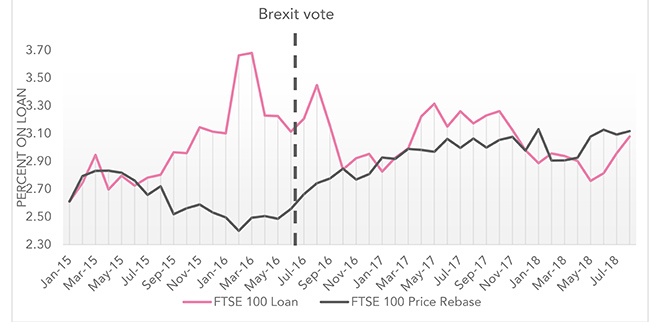

It is difficult to argue that the referendum held in June 2016 increased confidence and certainty in the UK capital markets. The outcome of the referendum clearly impacted the level of stock lending in UK Plc.

On the one hand, the more internationally focused, dollar-reliant FTSE 100 has seen a price increase and overall reduction in the amount of stock on loan since June 2016:

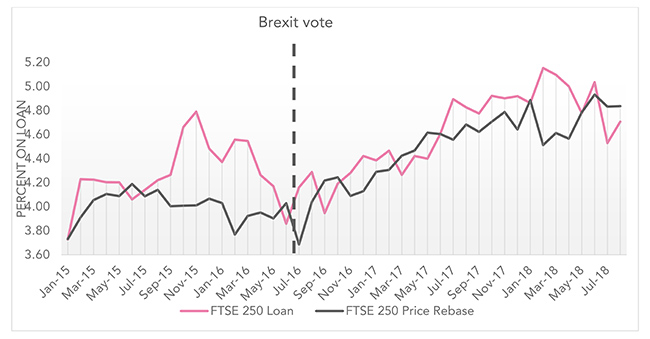

On the other hand, the FTSE 250 has also enjoyed a positive price performance since the referendum, yet with price rises here came an increase in lending:

The FSTE 250 chart above provides a stark view of market trends on lending and price when coupled with the historical P/E comparison, which shows increased earnings at almost the same rate as the price increases. The level of stock on loan is growing at the same rate as price. A weakened pound has damaged earnings for many FTSE 250 issuers since the referendum.

Shorting

This article has examined the level of stock lending in the UK market, with data sourced from Euroclear. The other side of the equation is shorting – where investors borrow shares and hope to make money from a price fall in that security. This dataset is less complete, with the UK’s Financial Conduct Authority (FCA) providing information to the market only where a short position is greater than 0.5 percent by any individual investor.

As at November 20, 2018 there were 609 disclosed short positions greater than 0.5 percent, totaling £13.4 bn. The biggest shorters in UK Plc were Marshall Wace with £1.4 bn, AQR Capital Management with £1.3 bn, and BNP Paribas with £925 mn in total shorts open and disclosed to the FCA. Globally, BlackRock held £896 mn in open short positions above 0.5 percent.

What IR can do when facing a heavily shorted stock

The main reason for an investor to open a short position in a stock is the belief it knows something negative about that stock that the market may or may not know.

The role of IR is crucial in helping companies counter short investors. Clear, consistent communication to the market is vital, as is delivering on promises.

When facing an investor with a large short position, it is advisable to offer a meeting, especially if it is not clear why it is shorting you. Many shorting investors will not accept a meeting with management or the IRO, but they could be open to meeting with the chairman or senior independent director. Investors that open a short position are always wary of a charismatic CEO who can talk himself/herself out of any situation.

Mark Robinson is head of EMEA issuer services at London-based RD:IR