This article was originally published by the Peterson Institute for International Economics, which retains copyright

The US-China economic confrontation of the last few years has prompted predictions that the world’s two largest economies are headed for a ‘decoupling’. US President Donald Trump’s administration’s recent threat to delist Chinese companies from US stock exchanges if they fail to comply with US accounting regulations underscored that possibility, and Trump tweeted in mid-June that ‘a complete decoupling from China’ was a US policy option.

But for all the fireworks over tariffs and investment restrictions, China’s integration into global financial markets continues apace. Indeed, that integration appears on most metrics to have accelerated over the past year. And US-based financial institutions are actively participating in this process, making financial decoupling between the US and China increasingly unlikely. An examination of the data shows the danger of generalizing based on misleading anecdotal evidence.

Regulatory reform in China has opened the way for foreign financial institutions

The best example of China’s deepening integration into global financial markets is the substantial increase in the role of US and other foreign financial institutions in China, made possible when Chinese regulators in 2019-2020 eased long-standing restrictions on ownership and other factors. Historically, foreign financial firms were largely restricted to operating in joint ventures with a minority ownership stake. Recent liberalization has led to a substantial increase in the number of majority or wholly foreign-owned financial institutions operating in China, including many US institutions.

The attraction of the Chinese financial market for foreign firms is substantial and will only grow larger. The size of China’s financial services market is $47 tn, but previous restrictions meant foreign firms have only a tiny slice of most sectors of this market – for example, less than 2 percent of banking assets and less than 6 percent of the insurance market. Given the large size of China’s domestic financial industry, if foreign firms can increase their shares in these market sectors, they stand to generate large profits.

Some examples of US financial institutions that have taken advantage of China’s recent liberalization in finance include:

- PayPal in 2019 acquired a 70 percent stake in the Chinese firm GoPay, making PayPal the first foreign company to provide online payment services in China. This allows PayPal to compete in the rapidly growing global mobile payments market, forecast by the market research firm Frost & Sullivan to reach almost $100 tn in 2023

- Goldman Sachs in March 2020 received approval to step up its 33 percent minority stake in its joint venture securities firm, Goldman Sachs Gao Hua Securities Co, to a 51 percent majority ownership. At the same time Morgan Stanley was able to increase its ownership stake in its joint venture securities firm, Morgan Stanley Huaxin Securities Co, from 49 percent to 51 percent

- JPMorgan in June 2020 received approval to operate a wholly foreign-owned futures firm

- Also in June, American Express received approval to be the first foreign credit card company to launch onshore operations in China through its joint venture with a Chinese fintech firm, allowing it to conduct network clearing operations. Visa and Mastercard have also applied to form network clearing licenses

- American credit rating companies have also recently gained increased access. S&P Global in 2019 set up a wholly foreign-owned firm that is the first licensed to conduct credit rating services in China’s domestic debt market. Fitch’s wholly foreign-owned subsidiary in May 2020 was approved to rate China’s onshore issuers, including banks, non-bank financial institutions and insurers and their bonds.

Cross-border capital flows into China have been increasing

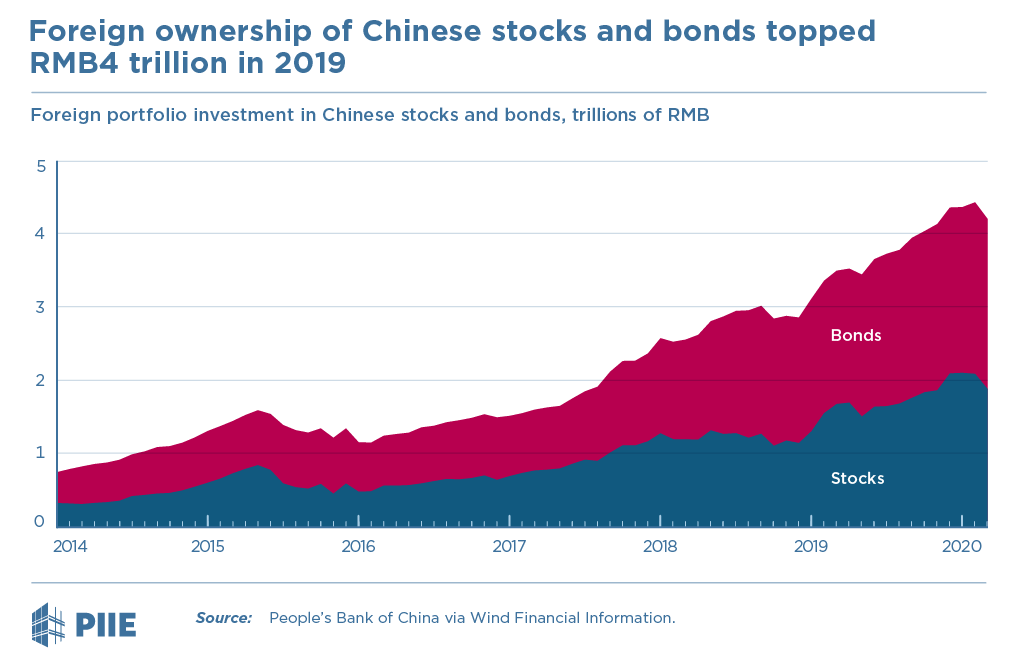

In addition to the increased presence of majority or wholly foreign-owned financial institutions, China’s integration into global financial markets is reflected in growing cross-border capital flows of not only foreign direct investment (FDI) but also of portfolio capital. The figure below shows the steady increase in foreign ownership of Chinese stocks and bonds, reaching RMB4.2 tn ($594 bn as of July 1, 2020) by the end of the first quarter of 2020. This amount is almost certain to grow over time as the US-based financial company MSCI and other major firms that provide global indices driving much institutional investing gradually increase the weight of Chinese listed firms in their indices.

American multinational firms have been active in direct investment in China, investing $14.1 bn in 2019, up from $12.9 bn in 2018. And while there has been much talk of US firms diversifying their supply chains, a March 2020 survey by the American Chamber of Commerce in the People’s Republic of China finds that more than 80 percent of US companies are not considering relocating their manufacturing out of China.

But FDI inflows into China, including by US firms, are likely to wane in 2020, with the United Nations forecasting global FDI to decrease by up to 40 percent as a result of slowing global economic growth caused by the Covid-19 pandemic.

The one sign of financial decoupling between the US and China is the sharp decline in Chinese direct investment into the US. After reaching a peak of $46.5 bn in 2016, it fell to only $4.8 bn in 2019. This drop reflected increased surveillance of inbound Chinese investment by the Committee on Foreign Investment in the United States and, more importantly, a sharp increase in the control of outbound capital by the Chinese authorities.

A pointless drive to delist Chinese companies from US stock markets

Denying Chinese companies access to US equity markets would be another sign of decoupling. Two motivations could lead to such denials. First, US regulators have not been able to access the working papers associated with the audits of Chinese firms listed on the US stock market. And there have been cases of accounting fraud that have resulted in losses for investors in Chinese companies in US markets. The most recent was Luckin Coffee. Second, it appears that some believe denying Chinese firms access to US capital markets would slow China’s growth.

Currently about 230 Chinese companies with a market capitalization of about $1.8 tn are listed on Nasdaq and the NYSE. On May 20 the Senate passed the Holding Foreign Companies Accountable Act, which, if passed by the House and signed by Trump, would require Chinese companies that fail to comply with the standards of the US Public Company Accounting Oversight Board within three years to delist. The president potentially accelerated this process when he charged Treasury Secretary Steven Mnuchin on June 4 to come up within 60 days with recommendations to protect US investors in Chinese securities, possibly setting the course for an executive order that would require delisting Chinese companies from US stock exchanges much sooner.

Denying access to US capital markets would not be a major step in decoupling and certainly would not slow China’s growth. First, much if not most of the capital raised by these Chinese firms on US stock markets has come from international investors, not US residents.

Moreover, delisting would not deny Chinese companies access to US capital. In fact, one method to accomplish delisting is through go-private investment transactions. For example, Warburg Pincus and General Atlantic, two major US private equity firms, led a deal in June to buy out the Chinese firm 58.com, which is listed on the NYSE. When the deal closes later this year, existing shareholders will be bought out at a premium price and the firm’s shares will no longer trade in the US. At that point, 58.com will have access to US capital through US private equity firms rather than through the public markets. The number of go-private deals of US listed private companies surged in the first half of 2020.

Second, many Chinese companies will delist by shifting their listings to the Stock Exchange of Hong Kong (HKEx) where both US residents and international investors can continue to invest. Already China’s largest semiconductor company, Semiconductor Manufacturing International Corporation, delisted from the NYSE in 2019 and now trades only in Hong Kong. The process of shifting from a US to a Hong Kong listing is fairly simple for larger Chinese companies: apply for a secondary listing in Hong Kong, build up enough trade volume to make the Hong Kong listing primary, then drop the US listing.

Alibaba, far and away the largest market cap Chinese company listed in the US, already gained a secondary market listing in Hong Kong in 2019. Two other Chinese firms, JD.com and NetEase, launched secondary offerings in Hong Kong in June this year. These firms are thus positioned to drop their US listings.

The key point is that the market for capital is global. Shutting out Chinese firms from listing in the US would not deny these firms access to US capital. US institutional investors and US residents who want to own shares in these companies will simply buy them in Hong Kong. Similarly, foreign investors that have invested in Chinese companies via New York listings will buy them in Hong Kong. The primary beneficiary of a US delisting policy would appear to be the HKEx.

Prohibiting US federal pension funds from investing in Chinese equities has no teeth

The US Federal Retirement Thrift Investment Board in 2017 decided to switch the index of funds covering the international investments of the federal Thrift Savings Plan (TSP), the so-called I Fund, from the MSCI Europe, Australasia and Far East Index to the broader MSCI All-Country Ex-US Investable Market Index, which includes a small slice of Chinese companies. The goal was to rectify the virtual absence of emerging market exposure in the I Fund, an anomaly among large retirement funds.

The international component of the TSP has about $50 bn in international equities. The planned shift to the broader index would have put about 8 percent of the fund, around $4.5 bn, into Chinese stocks starting in mid-2020. In response to pressure from the president and members of Congress, this decision was paused in May 2020 and seems unlikely to be revisited.

While this action to preclude Chinese stocks from the I Fund of the TSP attracted substantial attention, it is largely symbolic in the broader context of both the TSP and US investment in Chinese equities. A potential $4.5 bn of Chinese equity investment by the TSP is not much more than a rounding error relative to the $560 bn in TSP fund assets at year-end 2019. And it is also small relative to the estimated $260 bn in Chinese securities owned by US residents [authors’ estimate based on US Treasury data]. Finally, prohibiting TSP investment in Chinese stocks is completely irrelevant relative to the market capitalization of listed Chinese companies, which now stands at roughly $13 tn.

Nicholas Lardy