One short year ago, a year that felt like a decade to most of us, the Covid-19 pandemic had just begun to rear its ugly head. The only thing that seemed certain at the time was that these would be unprecedented times for the global economy and companies operating within it – and that our use of the word unprecedented would skyrocket.

As fate would have it, Covid-19 emerged in the weeks – and in some cases, days – after many companies had reported FY 2019 earnings and published guidance for 2020. In the blink of an eye, the only thing that seemed certain was the uncertainty that management teams spoke of repeatedly as they withdrew guidance. Corporate strategies and investor communications both pivoted to focus on preserving liquidity, eliminating non-essential Capex and looking under couch cushions for loose change. Many companies suspended or withdrew guidance in anticipation of material changes to their businesses.

Most published analysis has focused on the constituents of the S&P 500, which had varying degrees of immunity to the coronavirus (pun sort of intended). We elected instead to look across the 4,000+ companies listed on national US exchanges to identify trends more broadly applicable to our clients.

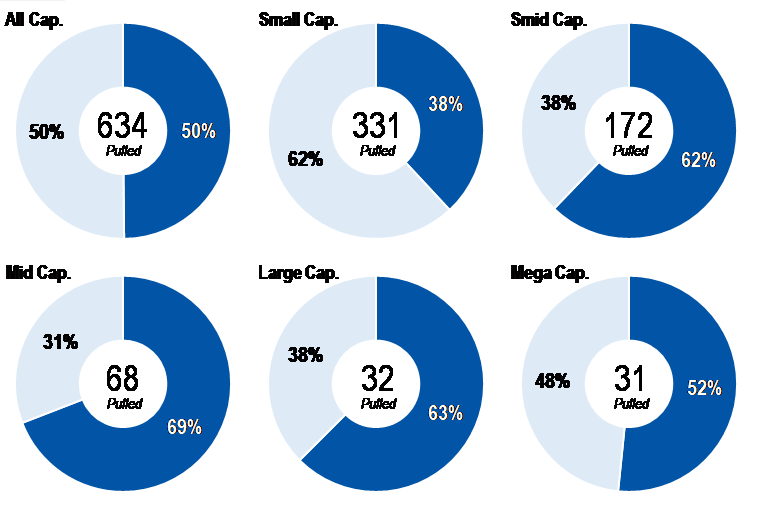

In total, 634 companies, or 58 percent of those that published guidance FY 2020 guidance in January, February or March of 2020, pulled it by the end of June.

Number of companies that issued 2020 guidance by month

Source: FactSet Research Systems; Rose & Company

Over the balance of the year, companies proved to be in no rush to reinstate 2020 guidance given the uncertain economic backdrop. One could argue that with an unprecedented recovery in stock prices in full swing, reinstating could only hurt, and over the course of the year very few companies did. Indeed, over the balance of 2020, there was virtually no difference in the average share price performance of companies that reinstated and those that didn’t.

Will the past be prologue?

Although Covid-19 is still with us, professionals and armchair epidemiologists alike think the worst is behind us. Let’s hope so. With enough light visible at the end of the tunnel, it’s an appropriate time to revisit guidance trends, particularly as most companies have reported FY 2020 earnings and either provided guidance for FY 2021 or not. We refreshed our data and, multiple Excel freezes later, are in the position to share some high-level analysis.

The data is pretty compelling. Of the 634 companies that pulled guidance in 2020, just 318 (50 percent) have provided guidance for 2021. For one reason or another, companies are thus far reluctant to guide for 2021. Consider that by the end of last March, 1,087 companies, or about 25 percent of the universe of 4,000+ companies we looked at, had issued guidance for the year. Jump forward 12 months and the number drops sharply to 813 (672 if you subtract the 141 companies that had not provided FY 2020 guidance as of March 31, 2020).

This decline is certainly notable, and we suspect that we will never revisit the peak level of guidance we saw last year (note: 2020 saw the greatest number of companies on record publishing full year guidance). Looking under the hood, we suppose there are no major surprises. The larger the company, the more likely they are to resume guidance. As noted above, larger cap companies were faster to reinstate 2020 guidance and have continued with the practice in 2021.

Breakdown of companies that pulled FY 2020 guidance

Source: FactSet Research Systems; Rose & Company

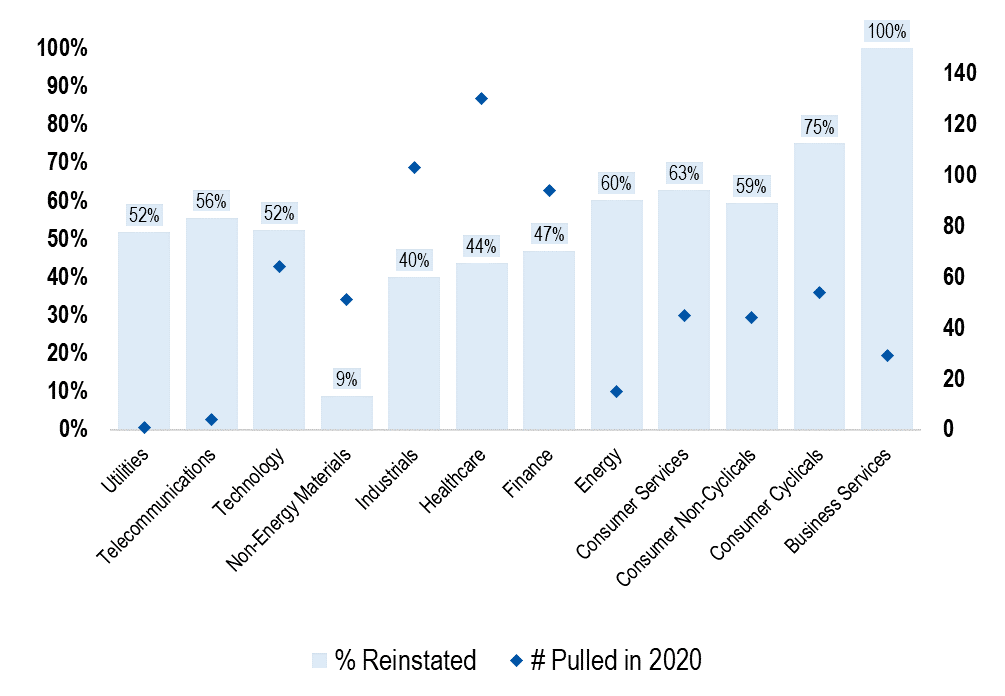

Here’s a snapshot of what we observed across different sectors.

Source: FactSet Research Systems; Rose & Company

Don’t look a gift horse in the mouth

The large drop in the number of companies issuing guidance could mean one of two things: the business climate is still simply too fluid to be certain about anything; and companies are reconsidering their disclosure practices.

We had previously put forth the idea that the (only) silver lining of the pandemic was that it presented companies with a great opportunity to alter the way they communicate with the investment community. Many companies spend too much time worrying about guidance and thinking about how to communicate it to the Street. We don’t love conventional guidance such as earnings per share, EBITDA and revenue for several reasons:

- Consensus estimates tend to overshoot guidance (analysts often think management teams are being intentionally conservative) and estimates never go down as quickly as guidance does. We have empirical data to show that companies that revise guidance downward consistently miss earnings

- The consequences of missing guidance can be meaningful in both the short and long-term, and management teams that are myopically focused on guidance may act in a way that is counter to long-term valuation creation

- Finally, long-term investors are less concerned about short-term performance and more focused on strategic execution.

We prefer softer guidance around business trends, where possible, and are certainly a proponent of limiting guidance to things such as selling, general and administrative and interest expense and Capex and other expectations that should be easy for most people to estimate anyway.

Those things are controllable to a large extent, without taking into account the intricacies of Gaap accounting. We suggest that companies should consider using this period when uncertainty is (still) acknowledged by most investors to cease the practice of providing financial guidance and instead provide sufficient information to help analysts build their models.

More importantly, we recommend that companies provide investors with a long-term roadmap focused on fundamental economic drivers of their businesses and long-term strategic goals. Use the opportunity to educate investors about core business drivers, and lay out a clear vision for long-term performance based on these drivers. Share management’s outlook or targets for KPIs tied to the company’s long-term strategic goals.

There are, of course, countervailing arguments and one company’s rationale for providing guidance may be just as good as another company’s rationale for not providing guidance. We can take that discussion up on a case-by-case basis. In any event, a shift in company communications may or may not be underway. We’ll let you know next year!