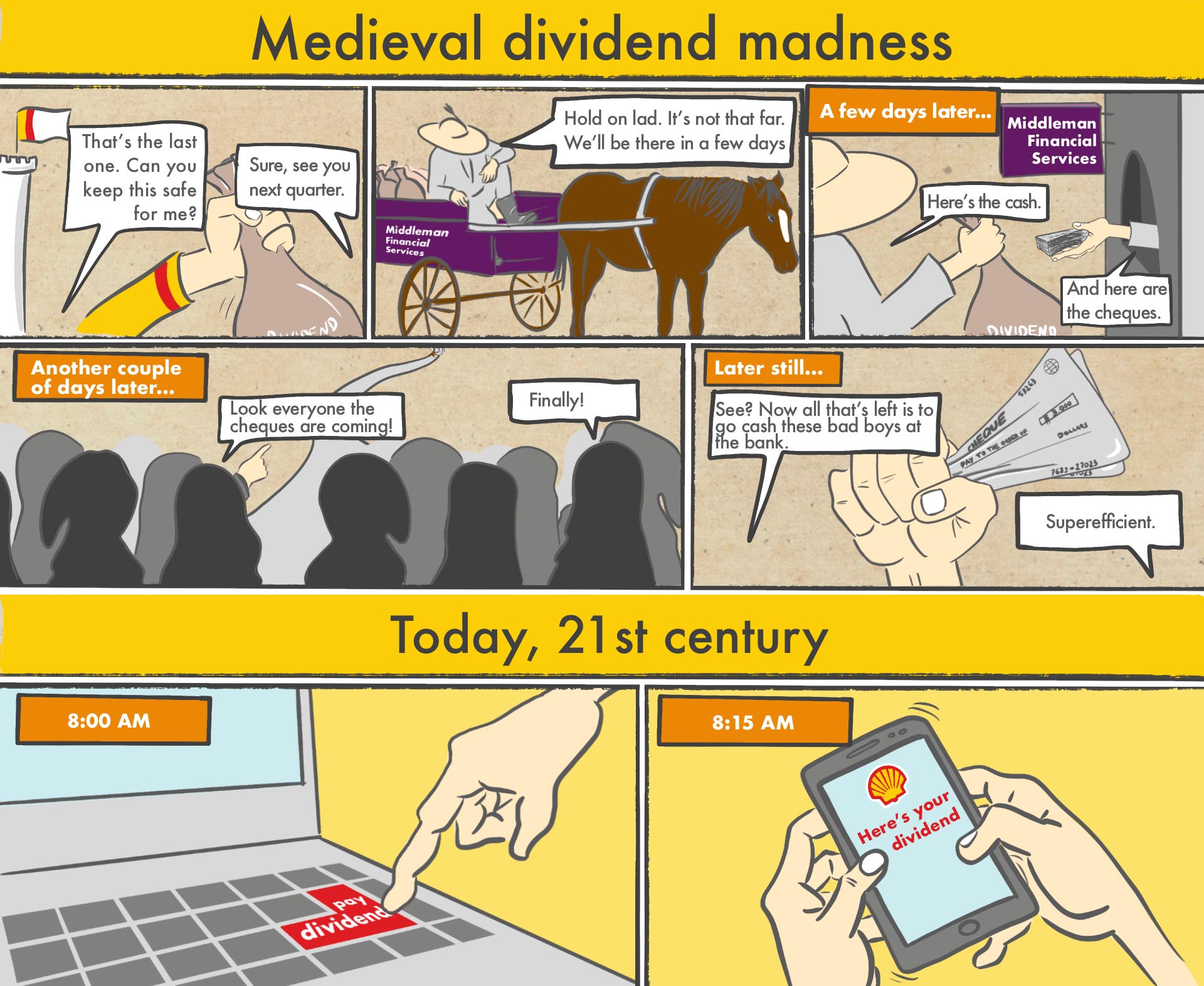

In hindsight, noting the benefits in terms of cost, hassle and fraud risk, it is surprising it has taken so long to retire the widespread use of checks. In 2005 Shell was the first retailer to stop accepting checks in the UK. Within a few years all other major retailers followed and now this antiquated practice has disappeared from the high street. Yet many FTSE corporates continue to use checks to pay dividends to their shareholders. In fact, until 2020 even Shell paid a large portion of its dividends via checks.

Not anymore. Having consulted the market, we overhauled our ways of working, resulting in the following real benefits:

- Better investors’ experience removing friction, foreign exchange and interest leakage, cost and risk

- Removal of unsecured, prolonged, multibillion credit exposures each quarter

- Better control and oversight via a new and proprietary infrastructure and reduced administrative cost (for example, we no longer need to post 150,000 checks each quarter).

In addition, streamlining Shell’s dividend distributions, even after its dividend reset, saves Shell upwards of millions in cash each year. This cash saving originates from preserved yield and reduced foreign exchange leakage, avoiding idle cash at our registrar and reduced administrative costs and banking fees.

This article explains the steps Shell took and how these benefits were delivered. Given the upsides, we hope the article encourages fellow FTSE constituents to follow suit.

1 Weigh in on your registrar’s arrangements

The benefits could not have been achieved if Shell’s investor relations team had not encouraged the company secretariat to team up with the treasury team to drive this transformation in dividend payment execution. This enabled a full overhaul of the registrar’s arrangements applying best treasury practices.

Distributing dividends represents a high-exposure business process, where even small improvements can make a material difference. Dividend distribution touches upon a wide range of treasury capabilities: cash management (including multi-currency cash management), counterparty risk, foreign exchange and dividend reinvestment. Therefore, it makes full sense for any treasurer to be closely involved in the arrangements struck between a corporate and its registrar. This also ensures any trade-off across the associated terms and conditions are made upon a sound economic basis acknowledging knock-on effects on investors.

As this ultimately trickles down to investors, any IR team may be keen to weigh in and ensure dividends find their way to all investors via the most optimal way.

2 Eradicate dividend checks

In 2021 there is simply no justification to distribute dividends via checks. For a corporate, checks are expensive, cumbersome and fraud-prone. There is a similar downside for investors and their custodians. The check is cut on a certain date, but until custodians have received it by post and cashed it, they have not received the dividend, exposing them to hassle, charges, lost interest and (credit) risk. To appreciate this, one should note that cashing in a check these days tends to involve various physical movements including typically two overnight flights to and from the custodian’s service center in central Europe. At each station along this almost 4,000-kilometer-long journey, each check passes through multiple hands.

While typically asset managers have agreed assured income provisions with their custodian, this comes at a cost to them and does not remove the residual clawback risk. We were simply not comfortable to associate Shell with such practice and eradicated checks fully.

Doing so represented a well-timed change. While Shell’s dividend checks always represented a considerable administrative headache, settling a multibillion dividend amid a Covid-19 lockdown via thousands of paper checks would have created havoc.

3 Distribute through central security depository

The UK’s central security depository, CREST, owned and operated by Euroclear UK & Ireland, provides a central bank-based cash distribution capability across pounds sterling, euros and dollars. This capability is by far the most robust and efficient way to distribute cash across investors. It is for this reason that custodians, holding practically all of the FTSE’s equity for investors, urge corporates to pay their dividends via CREST.

Fortunately, two thirds of FTSE 100 companies’ dividends are already paid via CREST. But this still leaves several FTSE constituents, including various dividend aristocrats, not yet doing so. Hearing the market feedback and noting the benefits, Shell is no longer among them, as we encouraged our registrar to adopt CREST. All three UK registrars are now perfectly able to distribute via CREST.

4 Employ real-time payment systems

While more than 95 percent of FTSE dividends can be received via CREST, the residual balance can be received only via bank transfers. This includes the certificate holders and the corporate sponsored nominee’s participants. For Shell this represents well over 400,000 individual payments each quarter.

Here, we opted to employ real-time payment systems across all three currencies, including Faster Payments combined with Chaps for pounds sterling and SEPA Instant for euros. This enables same-day settlement, avoids batch processing (as experienced with BACS) and provides instant feedback on each individual payment made.

5 Stop prefunding your registrar

Before, Shell prefunded its registrar. Every quarter, we wired most of our dividend a few days in advance. There was no benefit: once the cash left our account, we missed out on interest and increased the level of credit risk to our registrar and its own bank.

The full electronic settlement via CREST and real-time payment systems facilitate same-day settlement. This means we only part with the cash early on the payment day, while investors can still be confident of receiving their dividend on the same value-day.

6 Create win-wins via currency options

Going fully electronic also allowed us to expand the options available to investors. This made it possible for them to receive a dividend in dollars, when only pound sterling and euro payments were available before. We are an energy company predominantly receiving dollar revenues and therefore declare our dividend in dollars.

This dollar option benefits our investors, which include a prominent US constituency, as it allows them to receive their dividend directly in dollars and avoid the associated foreign exchange exposure and leakage. Equally, it offers benefits to Shell given our natural long position in the dollar, reducing the quantum of pounds sterling and euros that need to be sourced.

Depending on the currency denomination of your revenues and the residency of your investors, you may be able to create a similar win-win by adding the option of receiving dividends in dollars or euros.

7 Employ dividend election rights

To facilitate these currency options, we introduced the application of dividend election rights. Doing so represented the inauguration of this technology in the UK market. Shell was already familiar with dividend election rights, as we have been using them for 15 years in the Dutch market.

Election rights remove inefficiencies of the mandate-based election process, align with European market standards and allow investors to apply buyer protection to open positions. Therefore, it is no surprise the UK market has applauded us for taking this step.

8 Fund only payable dividends

Despite best efforts, there will always be a sizable group of shareholders that cannot be paid their dividend because they have not provided bank account details or their bank account has been closed down after their death. This is particularly relevant for certificate holders and private individuals holding their shares in CREST. Previously, we provided our registrar with funds to cover even for those shareholders who clearly could not be paid. In effect, this left associated cash idle at our registrar for at least 12 years, at which time the shareholders’ entitlement can be forfeited.

Now we provide cash only for those dividends our registrar can pay out directly. Any dividend that unexpectedly cannot be paid out contributes to funding the next quarterly dividend. This avoids leaving cash idle at our registrar and removes the associated credit risk and yield losses. Furthermore, it has enforced our administrative control over the unclaimed balance and improved our ability to reunite these shares and associated unpaid dividends with these holders or their heirs.

9 Own your dividend payment infrastructure

A streamlined, brand-new payment infrastructure was built to handle our dividend distribution all the way into CREST. We deliberately opted to hold all associated bank accounts and even the CREST receiving agents directly in our own name.

While our registrar continues to operate this infrastructure, ownership offers us greater control and increased transparency and oversight. It also avoids imposing any (intra-day) exposures on the registrar. Furthermore, it reduces our dependency on our registrar by reducing its role to merely an operator of our own infrastructure. Finally, taking title on these bank accounts made it possible for us to employ our own principal cash management bank for dividend distribution.

10 Involve your own principal cash management bank

We opted to extend the involvement of our own principal cash management bank, Citi. Firstly, this brings superior payment technology across all three currencies and a proven global product capability and execution track record. Secondly, it allows for contracting these services under our own framework agreements, capturing economies of scope and scale (for example, reduced banking charges) for our own benefit.

Extending Citi’s involvement up to our shareholders’ doorstep made all associated transfers intra-bank. This allowed for overnight processing and thus facilitates earlier settlement on payment day while avoiding any credit concerns for the bank.

Cross-collaboration across Shell, our registrar Equiniti and our principal cash management bank also further strengthened Equiniti’s capabilities.

Royal Dutch Shell dividend – in numbers

- $1.3 bn per quarter

- Paid out in euros, dollars and pounds sterling

- Optional third-party dividend reinvestment programs (Drips) available in the Netherlands, UK and US markets

- 500,000 individual settlements per quarter

- Employing instant payment systems: Faster Payments, Chaps, SEPA and (FED) Wires

- All executed within a couple of hours

Dividend distribution: How is it done?

On average, each Royal Dutch Shell share is sold (and therefore bought) once a year. This means our shareholder base is subject to constant change. For this reason, for each dividend a ‘record date’ is defined at which point a picture is taken to establish how many shares each holder should receive a dividend for.

Once this picture is taken, these holders can elect to receive their dividend in euros, pounds sterling or dollars and ensure they can be paid (by setting themselves up to be paid via CREST or by providing their bank account details). Alternatively, they can opt to reinvest their dividend via one of the Drip offerings Shell allows to tag along as an additional election possibility for investors. These choices determine how much in euros and pounds sterling Shell’s treasury needs to source. Finally, on the payment day, each holder receives the dividend in the currency requested fully electronically.

A cartoon created by Shell to explain the dividend change

A cartoon created by Shell to explain the dividend change

About the authors

Paul Vos (paul.vos@shell.com), senior manager of treasury and corporate finance, and Anthony Clarke (anthony.clarke@shell.com), deputy company secretary at Shell, are available to provide further details.

An earlier version of this article appeared on June 10, 2021 in The Treasurer, the magazine of the Association of Corporate Treasurers, which can be found here

Anthony Clarke