Investor engagement well ahead of annual meetings has substantially increased

Proxy season kicked off with a flurry of headlines this spring about investor revolts. Shareholders in the United States loudly voted down Citigroup chairman Vikram Pandit’s $15 million pay package, and days later, investors on the other side of the Atlantic forced Barclays’ chief executive to forego £2.7 million in order to avert a similar public debacle at the company’s pending annual meeting.

Soon after, Andrew Moss, chief executive of the British insurance giant Aviva, resigned after 59 percent of investors rejected his compensation report.

Perhaps the more telling indication of growing investor muscle, however, is a story that may surprise many – the under-the-radar, largely successful campaigns to win over investors by a handful of companies that saw their pay packages go down in flames in 2011.

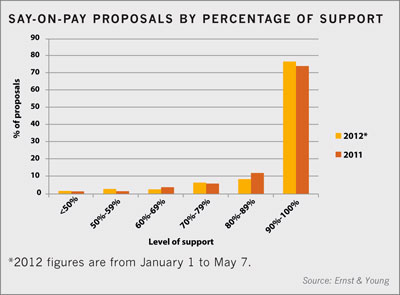

At least five prominent major companies who became poster children for out-of-touch executive pay last year garnered more than 90 percent support for new pay packages from their shareholders in the early days of the 2012 proxy season – a stunning turnaround that appears to reflect aggressive outreach to investors from companies previously viewed as unwilling to compromise.

At the top of the list is Umpqua Holdings, which saw its support rise from 35 percent to more than 95 percent. Stanley Black & Decker’s shareholder support rose from 39 percent to 94 percent, and Beazer Homes saw its totals rise from 46 percent to 95 percent.

Even Jacobs Engineering – the first company last year to have its plan voted down – came out on top, its numbers rising from 54 percent opposed to 95 percent in favor.

Reaching out

Ron Schneider, senior vice president at Phoenix Advisory Partners, attributes a major part of the turnaround to aggressive post-meeting investor outreach by all these companies.

‘The companies knew what the main drivers were and most had negative proxy adviser recommendations,’ Schneider says. ‘They did a lot of post-meeting engagement with investors to get an idea of their concerns, and the results were very, very notable.’

Schneider says that Phoenix worked with Umpqua – which had the largest percentage turnaround thus far for 2012 – for the first time in the months leading up to Umpqua’s recent meeting.

This engagement reflects a larger trend. A number of observers say they have noticed a significant uptick in outreach to shareholders this year – efforts that, though difficult to quantify, may well be unprecedented in size. ‘We are seeing a lot of outreach even before the votes are cast,’ says Amy Borrus, deputy director of the Council of Institutional Investors (CII). ‘I don’t have any numbers to point to, but it just feels that way, more than before. Particularly on compensation, more companies are engaging shareowners ahead of time. They are also trying to get ahead of ISS recommendations. More are filing responses.’

‘We are seeing a lot of outreach even before the votes are cast,’ says Amy Borrus, deputy director of the Council of Institutional Investors (CII). ‘I don’t have any numbers to point to, but it just feels that way, more than before. Particularly on compensation, more companies are engaging shareowners ahead of time. They are also trying to get ahead of ISS recommendations. More are filing responses.’

Companies are ‘looking around at their peers’, says Schneider, and ‘if they see somebody doing something innovative on disclosure and clarity, they are adopting those methods. Best practices are emerging and many companies are upping their game.’

Sanjay Shirodkar, of counsel at DLA Piper, agrees, noting that this year many companies have begun ‘front-loading’ the discussion of executive compensation in filings not previously known as easy reads. They’ve added user-friendly charts, graphs and executive summaries in an effort to make sure their rationale is clearly understood.

The trend is only likely to continue as the consequences for failing to adequately sell compensation plans continue to grow. ISS is moving ahead with plans for a ‘yellow card, red card’ system, which draws its analogy from the penalty system of soccer.

Failing a say-on-pay vote is a warning, or yellow card. Failing to address a failed say-on-pay vote is a red card, or penalty, which may well result in a recommendation by ISS of a ‘no’ vote against members of the corporate compensation committee.

ISS announced recently that in 2013, any company that receives less than 30 percent support for say on pay and that fails to address concerns is likely to receive recommended ‘no’ votes on directorships.

Not to be outdone, advisory firm Glass Lewis came out with its own even more stringent plan soon after, announcing that it will do the same for companies that receive less than 35 percent.

Board elections receive more attention

The issue of whether to hold annual board elections has been another hot topic this year. Professors at Harvard University Law School, led by Lucian Bebchuk, the director of the school’s Program on Corporate Governance, have been working with pension funds and other large investors to file resolutions with a number of companies that still have staggered elections, singling out about a third of those that remain.

Of 60 petitions filed, 44 were withdrawn after the companies voluntarily agreed to change their policies, says Tim Smith, senior vice president of Walden Asset Management, who adds that the 12 votes that occurred midway through the proxy season averaged a tally of 79 percent in support.

‘A couple of years ago, this issue was being hotly debated,’ Smith says. ‘Now it has overwhelming investor support. Companies read the tea leaves, and this is a case in point of how things can change dramatically. It’s become a litmus test for good governance.’ While not willing to concede that annual votes are now the only standard, Shirodkar acknowledges that the deals reached with 44 of the targeted firms were ‘a fairly significant victory for shareholders’.

While not willing to concede that annual votes are now the only standard, Shirodkar acknowledges that the deals reached with 44 of the targeted firms were ‘a fairly significant victory for shareholders’.

One thing seems hard to deny: those that fail such ‘litmus tests’ are increasingly coming under attack. Already this year, some investors have demonstrated a new level of willingness to target directors.

This year, Borrus says, has been notable for ‘lots of activity from other than the usual suspects. More mainstream investors are speaking out. This has been an extraordinary year, with shareholders demanding more accountability from the board.’

Chesapeake Energy has received letters from hedge funds demanding the board oust the company’s co-founder and chief executive, while the company’s largest shareholder, Southeastern Asset Management, has demanded that Chesapeake consider offers from those interested in acquiring the company. Southeastern has also demanded more oversight of the board at Olympus, where it owns a 5 percent stake.

No hospitality for shareholders

This year, for the first time, six sizeable public employee pension funds that belong to the CII singled out nine boards that had failed to heed non-binding shareholder proposals which had previously won majorities during annual meetings.

Among them was Hospitality Properties Trust (HPT), a real estate investment trust, which had ignored majority shareholder votes in favor of board declassification for three consecutive years.

The CII held an April 17 conference call with the company. Borrus will not disclose what transpired on the call, but CII members were apparently so disappointed that they decided immediately after the call’s conclusion to pay solicitation fees and target two of the board members for removal.

At the company’s annual meeting, independent trustee Bruce Gans received just 42 percent of the votes cast. The other director up for re-election, managing trustee Adam Portnoy, garnered 53 percent of the vote.

Gans resigned, but in what Borrus calls ‘an extraordinary affront to shareholders’, the board immediately reappointed him to fill the vacancy.

Tim Bonang, vice president of investor relations for HPT, says that a de-staggered board ‘encourages short-term thinking’. In addition, he notes, HPT is chartered in Maryland and has a headquarters in Massachusetts, both states that require staggered boards. De-staggering the board would be ‘costly’ and might require the company to move, he says.

Bonang says CalPERS had been the driving force behind the declassification effort of the previous three years, in what may well be an attempt to pressure the board to demand that the hotels HPT owns use union labor.

‘It’s been pretty clear that we have been under pressure to persuade our operators to use union workers,’ Bonang says. Of the board’s decision to reappoint Gans, he explains: ‘It was the board’s belief that the vote against Dr. Gans wasn’t directed specifically at him for any personal failing, but was rather aimed at the board for specific proposals.’

In April, Ricardo Salgado, chief executive of Portugal’s biggest bank, Banco Espirito Santo, resigned his directorship at NYSE Euronext after failing to win a majority of votes at the exchange operator’s annual meeting. Salgado was absent at 75 percent of board meetings last year due to his own bank’s challenges during the European financial crisis.

Midway through the proxy season, ISS has voting results for 4,668 directors in the Russell 3,000. Of these, ISS recommended ‘no’ or withhold votes against 290, or 6.2 percent.

Of those, only Salgado failed, while another five directors received less than 50 percent but passed anyway – including two each at Graco and Barnes Group and one at Ferro – presumably due to plurality vote standards in place at those companies. Another 67 directors at 46 companies garnered between 50 and 70 percent of the vote.

The votes drive home the point that ‘the election of directors is no longer just a routine item’, says Schneider. ‘At this point, the number of directors who received less than 50 percent support from their shareholders is in the single digits – but you’ve got dozens more votes that were still uncomfortably close.’

Proxy access battle continues

This year’s results again highlight the renewed muscle of shareholders, a trend that can be attributed in part to the overall environment but which also stems from the end, two years ago, of rules that gave brokers wide latitude to vote on behalf of their customers, Schneider says.

This year’s annual meetings have also been notable for a number of battles over proxy access – rules that would require corporations to include shareholder-nominated board candidates in their proxy materials, rather than requiring shareholders to shoulder the often prohibitive cost of paying for their own proxy materials.

Last July a federal appeals court in Washington DC struck down an SEC rule that would have required proxy access, but the legal decision did not prevent an SEC revision to another related regulation – Rule 14a-8 – from taking effect.

This revision allowed shareholders, for the first time, to use company proxy materials to propose their own board election and nomination procedures. As a result, at least two dozen companies received shareholder proposals aimed at requiring proxy access.

The proposals varied widely. While the consensus ownership threshold established in the SEC proposal would have required those nominating directors to own 3 percent of the company for three years, some of the investor proposals suggested a threshold of just 1 percent. Others proposed a plan by which 100 shareholders or more with $2,000 worth of stock could band together to reach a threshold.

Few of the key votes had been taken yet by mid-season, but early results are noteworthy. At Wells Fargo, a proxy access proposal garnered 32 percent of the vote – an ambiguous number seized on by opponents and proponents alike as a victory.

At Hewlett-Packard, meanwhile, investors pushing a proxy access proposal agreed to remove it from the ballot after the company relented at the eleventh hour and agreed to implement proxy access in 2013 for shareholders who meet a 5 percent ownership threshold. At Ferro, a proxy access initiative that would have set a threshold at 1 percent was soundly defeated.

Patrick Quick, a partner at Foley & Lardner who specializes in corporate governance and proxy statements, says that ‘right now the battle is being won by those who oppose proxy access. But the question is: how will the war turn out?’

The SEC’s proposals, Quick notes, had far higher ownership requirements than some of those offered by proxy access proponents.

‘The activists and others now have the benefit of some shareholder reactions as well as input from the SEC,’ he says. ‘In 2013, will they get their acts together and come back stronger and better?’

Shareholder engagement can help boards secure supportWith board responsiveness to shareholders increasingly becoming an evaluation of director performance, constructive dialogue with investors around key topics of interest can help secure board support as well as leading to shareholder proposal withdrawals. |

This article originally appeared in Corporate Secretary, IR magazine's sister publication.